.png)

In DSCR Loan appraisals, the appraised value utilized is the “as-is value,” or the value based on the state of the property on the day that the appraiser visits and evaluates it. However, if the appraiser identifies significant repair needs or deferred maintenance, or the property’s original construction or major renovation is not yet completed, they may issue a “subject-to” value. This is essentially saying the valuation is valid only if specific repairs are completed before closing.

The common threshold is approximately $2,000 in deferred maintenance. Crossing that line signals problems that go beyond cosmetic issues and materially affect habitability, safety, or marketability, or what DSCR Lenders essentially care about: the ability for the property to generate income (through rental), on day one of the loan term.

The key is feasibility and timing: most subject-to findings involve repairs that can be fixed in a matter of weeks and verified with a re-inspection. But time is tight. Appraisals typically expire within 90–120 days, so borrowers must complete the repairs (or have sellers complete the repairs if an acquisition), schedule the re-inspection and return the updated “as-is” certification to the lender while the appraisal is still valid. Delays can mean added costs, re-inspection fees (another $150 to $250 typically), or in the worst case, having to order a completely new appraisal.

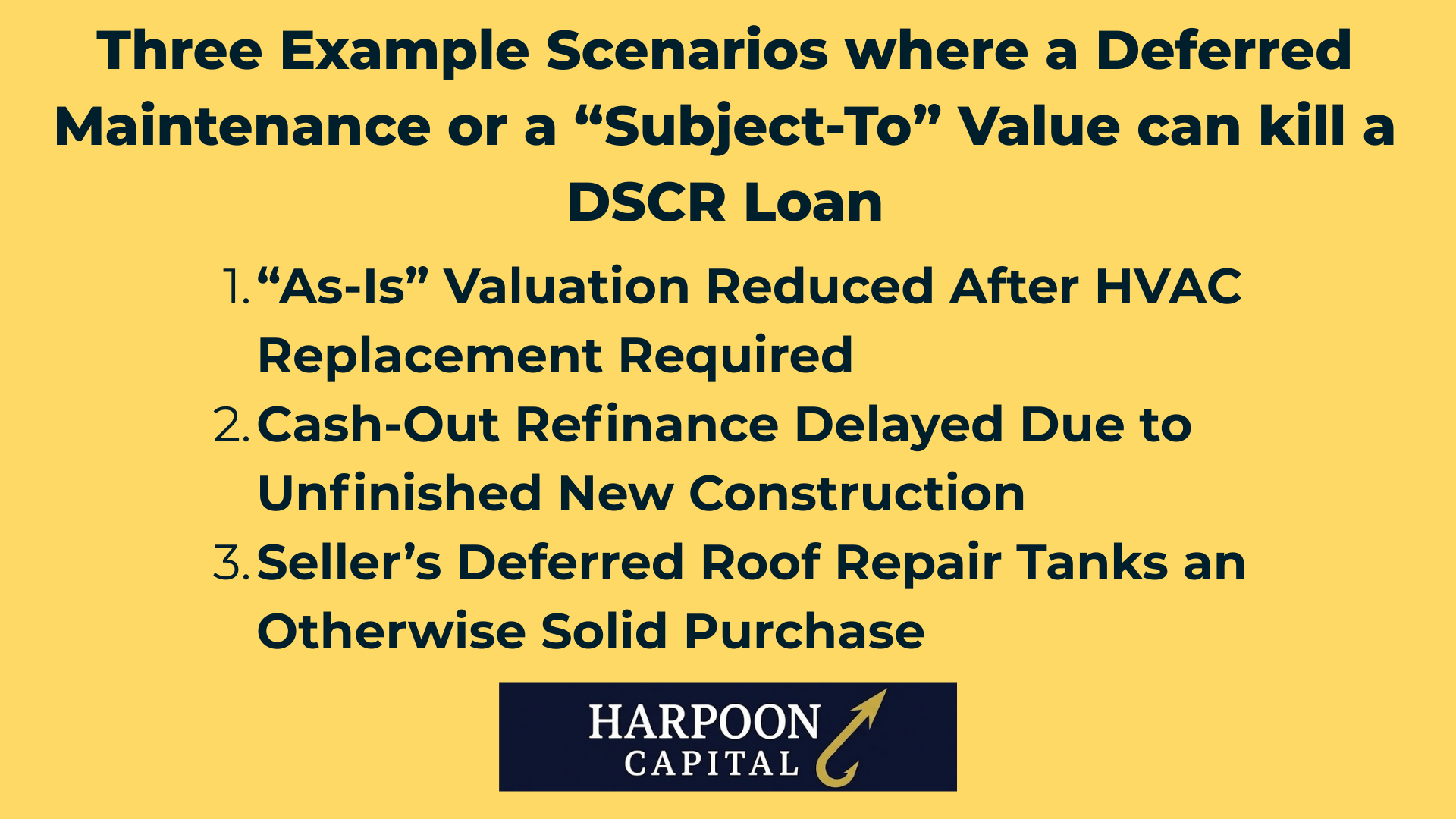

Here are three examples of this common DSCR Loan obstacle where the appraisal report can jeopardize a deal, not through a low appraised value, but rather through a finding of deferred maintenance past the standard limits ($2,000) or by only being able to provide a “subject-to” value, requiring some actions to get to the needed “as-is” valuation.

An investor goes under contract to buy a triplex for $720,000, expecting a $540,000 DSCR Loan at 75.0% LTV. During the appraisal inspection, the appraiser notes that one of the two outdoor HVAC compressor units is inoperative and requires full replacement, with estimated costs of $9,000. Because the system serves one of the three units, the appraiser classifies the issue as material deferred maintenance and reduces the “as-is” value to $705,000, stating that the $720,000 valuation applies only on a “subject-to” basis once the HVAC is replaced and verified.

DSCR Lenders cannot lend on “subject-to” conditions unless the repairs are already completed and re-inspected before closing and likely won’t proceed with the DSCR Loan even on the lower value accounting for the HVAC issue. The borrower either has to front the repair, delay the closing for a reinspection, or renegotiate the price, all of which can stall or kill the deal.

A builder-investor applies for a DSCR Loan refinance on a newly constructed duplex, expecting a $600,000 loan at 75.0% LTV based on an estimated $800,000 valuation. However, when the appraiser arrives, several elements of the building remain incomplete, specifically, the upstairs flooring is not installed, one bathroom lacks plumbing fixtures, and final electrical inspection hasn’t been signed off on. Because the property is not yet “rent-ready,” the appraiser issues only a “subject-to” value of $800,000 based on the value once these final touches are completed, and declines to provide an “as-is” value. DSCR Lenders require a property to be fully complete, habitable, and ready for occupancy before funding, with a final certificate of occupancy (CO). The DSCR Loan cannot proceed towards close until completion, reinspection, and reissuance of a CO.

A buyer (borrowing through a DSCR Loan) agrees to purchase a single-family rental for $430,000 with plans for a $322,500 loan at 75.0% LTV. The seller, who has owned and occupied the home for over 25 years, admits the roof hasn’t been replaced since the early 2000s but refuses to make repairs before closing. The appraiser notes “shingle curling and active leaks in attic,” estimates $12,000 for replacement, and values the property at a $430,000 “subject-to” value once the new roof is installed, tagging the $12,000 as deferred maintenance. The long-time homeowner’s reluctance to invest in a major repair turns what looked like a clean turnkey rental acquisition into a financing headache and possible deal-killer, and the buyer (borrower) can’t close a DSCR Loan to purchase the property with the $12,000 repair and subject-to value in the deal’s appraisal.

The reality of real estate investing is that rental properties will always have issues. Unlike the digital world, the real world is full of wear and tear and all that comes with that. Long-time investors in real estate will always have a long list of repairs and problems that were solved along the way. So, a finding of deferred maintenance or a “subject-to” value requiring some physical action items shouldn’t be too alarming or distressing – or else you are probably in the wrong business.

These are serious issues that can derail DSCR Loans and cost time, energy and money. Tactically preparing to prevent or minimize them is essential, and knowing how to best respond if and when they do inevitably come up is key for a long-term real estate investor. Here are three tips on how to prevent and potentially overcome this common DSCR Loan obstacle.

The most effective way to handle subject-to or deferred maintenance issues is to prevent them from being flagged in the first place. A key tactic to prevent this obstacle is to get a property inspection as soon as possible, and well before ordering the appraisal. Smart investors will hire a trusted inspector who understands what types of issues appraisers and lenders care about. Catching items like HVAC not working, missing handrails or active roof leaks early allows you to correct them before the appraiser ever steps foot on the property.

While property inspections are a part of almost all acquisition transactions, they can be hired for refinances as well. Hiring one, and spending the money, typically around $500, which is not nothing, but likely not too much, can be the smartest way to prevent these sorts of deferred maintenance or subject-to surprises. And even if the inspector doesn’t find anything that will prevent a smooth as-is appraised value, they will typically find some things that can be repaired, and the cost of a periodic inspection will likely typically pay for itself many times over through catching things that may become serious issues later on down the road before they can do so.

Even with the best preparation, most investors will eventually face a repair that needs to be addressed before closing a DSCR Loan. The investors who navigate these issues smoothly are the ones who already have trusted local vendors lined up, not the ones scrambling to find a roofer, HVAC tech or general contractor on short notice. Having a ready list of reliable professionals in the market area who can quickly produce bids, complete work, or even provide repair verification documentation can make the difference between closing on time and watching a deal fall apart.

This is where the tradeoff between long-distance real estate investing and focusing on specific markets comes into play. Chasing the best numbers or hottest emerging markets across the country can open doors to better cash flow and diversification, but it often comes with the hidden cost of having no local infrastructure when a problem arises. In contrast, focusing on a handful of markets you know well, where you’ve built a dependable vendor network, understand urgent timelines and have contractors who can prioritize your jobs, can dramatically increase execution speed and reliability. The result is not just fewer “subject-to” appraisal surprises, but also faster turnarounds when inevitable issues appear. The ability to have someone “on call” in cases of deferred maintenance or subject-to appraisals, that will communicate and execute the fix quickly and affordably, is the best way to overcome this particular DSCR Loan obstacle.

An additional best practice for overcoming an appraisal with a subject-to value or deferred maintenance may not be obvious, but should be very effective. If the appraisal comes back with these conditions, there are several pathways and solutions to solve it, but what might be just as important, is borrower behavior on the “needs list” and other items on the rest of the loan file. Many DSCR Lenders have busy operations teams, and are constantly juggling lots of deals and timelines, loans in different stages and with different issues and nuances that are popping up. That means that the lender is likely balancing prioritization of underwriting and processing, typically with focus on the loans that are most likely to be the quickest to close.

As such, if a DSCR Loan in process receives a “subject-to” appraisal or deferred maintenance, this is unfortunately typically a green light for “de-prioritization” of a loan file from the DSCR Lender’s operations team, i.e. if there are now doubts that the loan will make it to close, or if the fixes or property completions are indicating another few weeks of timeline, the reality is that the loan will likely move down the prioritization list – “pencil’s down” – in industry lingo. The result will likely be that the underwriting team’s precious hours and time moving to other loan files until a clear resolution is made.

While some of this is unavoidable, and there’s nothing a borrower or lender can do if there is a physical fix that takes time, borrowers can make an impact in this area by being extremely proactive with everything else. That means that while a needed fix or project is planned to bring the appraisal up to “as-is” or erase the deferred maintenance, everything else on the needs list should be quickly and neatly tackled, so that the loan file is pristine and complete in every way other than the pending appraisal update. It is very likely that these proactive actions will be not only greatly appreciated by the DSCR Lender’s operations team, but can also play a huge role in pushing the loan back up the lender’s prioritization list, so everything is “ready to go” as soon as the 1004 appraisal update is received, and the timeline havoc of the findings is fully minimized.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.