.png)

The next stage of a typical DSCR loan process involves when an investor is ready to move forward with an official application and formal authorization for the lender to pull credit (a “hard pull” with a full credit report for each guarantor). This typically occurs after the quotes and any pre-qual letters have been received and the investor is comfortable with the options on the table, and in cases of acquisitions, has the property under contract and the transaction lined up. In cases of purchase, this usually means that the buyer and seller have each signed an official sale agreement, typically called a “Purchase and Sales Agreement” (“PSA”) that spells out terms of the transaction but also importantly, transaction timeline, usually around 30 days. This means that once the PSA is fully executed, the clock immediately starts ticking on lining up everything to make sure the DSCR Loan is ready to close and fund in concert with the property sale - and speed in the process becomes front and center.

While different DSCR Lenders will offer different versions of DSCR Loan applications, the information required will largely be consistent and include the same general requirements. A loan application for a DSCR Loan will typically take around 15 minutes to complete, give or take the complexity of the scenario and each lender’s unique process. Generally, you will need to provide brief information on the investment property such as address and tenancy, the estimated financial, credit and experience of the borrowers or sponsors, loan request details like loan amount and terms requested, entity information if you are utilizing an LLC or trust/corporate structure to borrower and finally a declarations page that includes optional demographic information and signed declarations about knowledge of citizenship/visa status and any potential significant past or current credit issues.

Some DSCR Lenders will use what is called a Uniform Residential Loan Application (“URLA” or “1003 Form”), which is the same standard application used for conventional loans and crafted by Fannie Mae. This is especially likely for DSCR Lenders that offer DSCR Loans in addition to more traditional options, including conventional loans and other DTI-based non-QM loan types.

Q: Is a DSCR loan considered a non-QM mortgage?

A: Yes, DSCR Loans fall under the umbrella category of non-QM, or “non-qualified” mortgage loans. While all DSCR Loans are Non-QM Loans, not all Non-QM Loans are DSCR Loans; other Non-QM Mortgage Loans include loans commonly called “Bank Statement Loans” or “Asset Depletion Loans” based on their alternative qualification requirements, still based on DTI, but not qualifying under conventional Fannie Mae rules and guidelines.

While using the standard 1003 Application for a DSCR Loan has some advantages, such as familiarity and consistency and the ability to potentially present different quote options not only within DSCR Loan structures but other potential loan types the borrower may qualify for, there are some downsides as well. For one, there is information included on the 1003 that is not relevant for DSCR Loans (such as personal employment and income information), which can be confusing and extra paperwork and time spent for investors (who, like most of humanity, tend to strongly dislike both things!).

Additionally, there are things that can be crucial for DSCR Loan terms and qualifications that aren’t included on the 1003 such as entity information or other corporate ownership structures or details on tenancy and usage (like if it’s an STR). For that reason, a tailored DSCR Loan application that both includes extra information needed for DSCR Loans like entity information and rental strategy (i.e. LTR vs. STR) and does not include extra paperwork and sections that aren’t relevant to DSCR Loans, like income and a comprehensive financial assets liabilities list, is ideal.

Additionally, many top DSCR Lenders are not only tailoring their loan applications to be investor friendly by limiting items to only what’s needed, but also utilizing technology so that applicants can fill out the application electronically only, through an online application that minimizes confusion and unnecessary sections. For most lenders, gone are the days of having to worry about printing and scanning, or having to call your representative to see what sections you need to fill out and what you can skip – the processes are getting easier every day for a smooth application process, and DSCR Lenders, mostly private lenders not beholden to government-sponsored systems or over-regulated bank bureaucracies, can adapt to the 21st century much quicker.

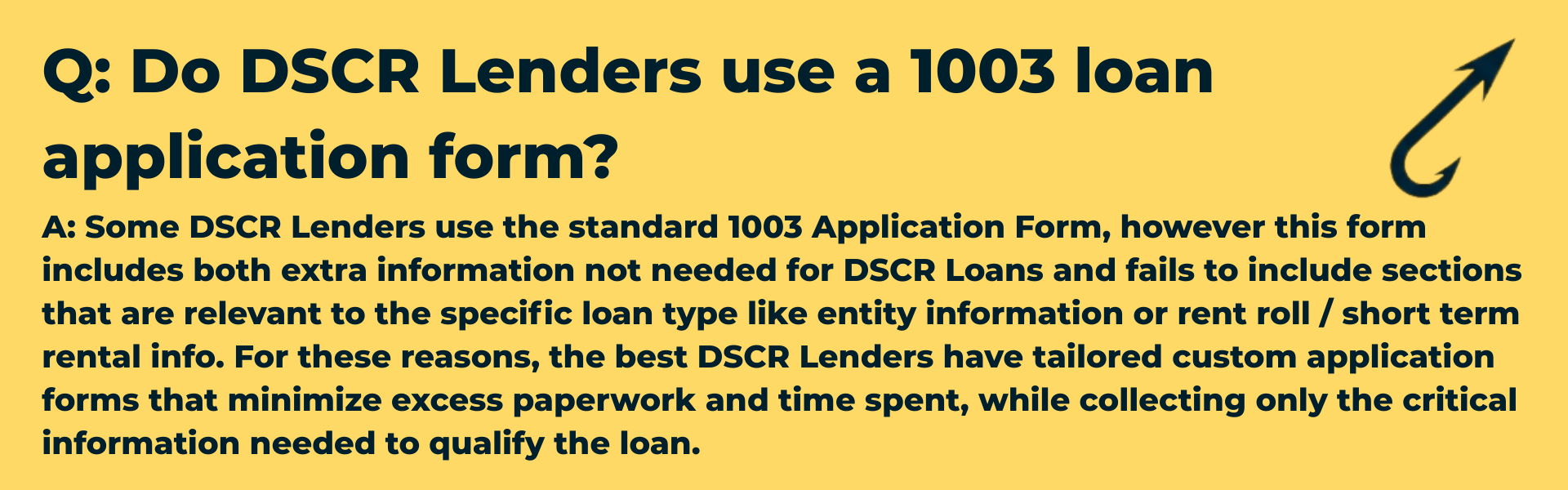

Q: Do DSCR Lenders use a 1003 loan application form?

A: Some DSCR Lenders use the standard 1003 Application Form, however this form includes both extra information not needed for DSCR Loans and fails to include sections that are relevant to the specific loan type like entity information or rent roll / short term rental info. For these reasons, the best DSCR Lenders have tailored custom application forms that minimize excess paperwork and time spent, while collecting only the critical information needed to qualify the loan.

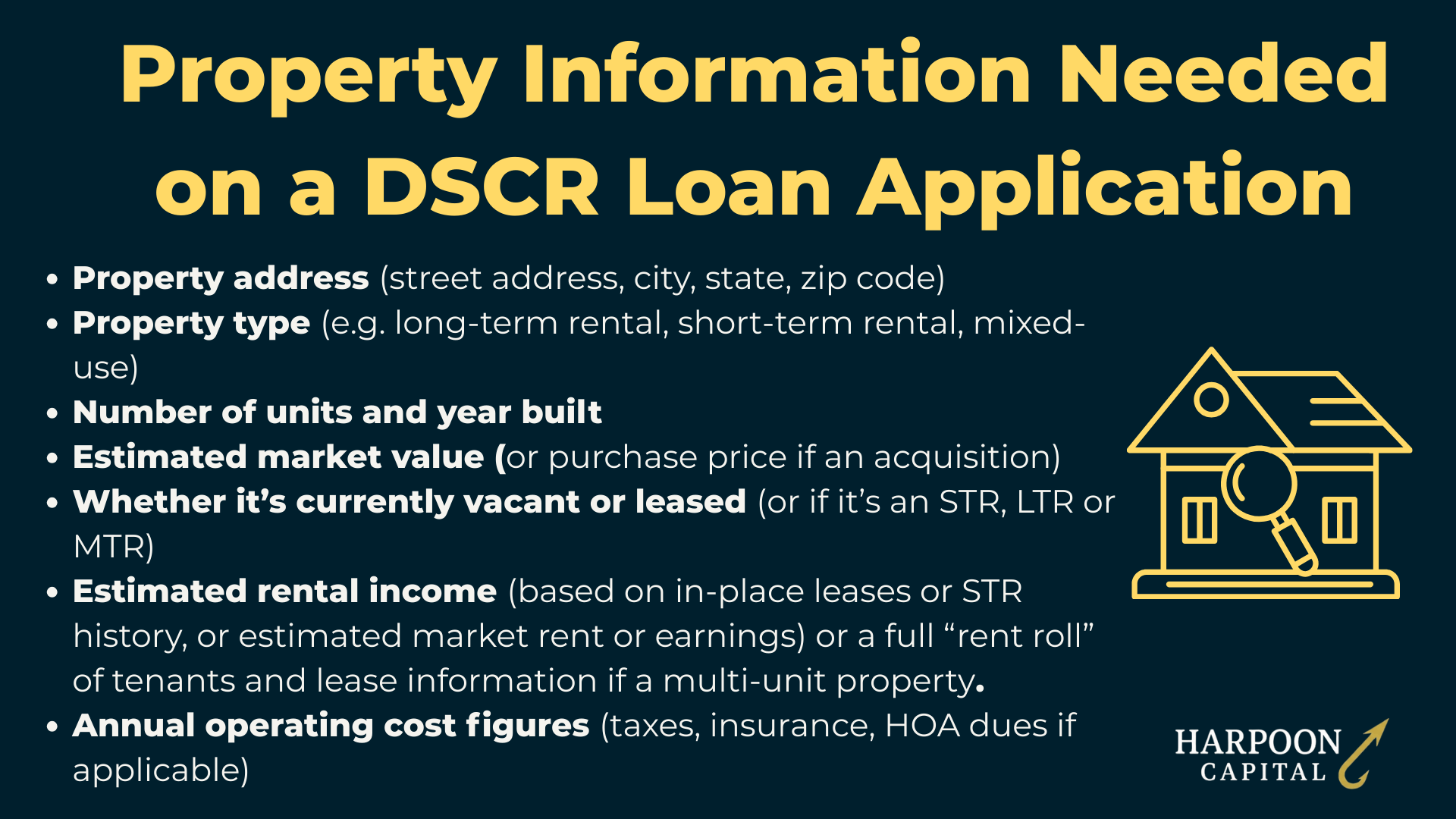

Below is a breakdown of the main components you'll typically be asked to complete on a DSCR loan application for lenders that use optimal DSCR-specific applications:

You'll need to provide the full details of the property you're financing, including:

You will also provide information on your personal credit and financial profile, including:

After likely reviewing quotes that include multiple options in terms of loan size and structure, the application will likely have a section on the specific loan terms being requested. This section is still malleable throughout the process, but picking specific terms to start is typically part of the application stage:

Q: Are DSCR loans available for cash-out refinancing to pull out equity?

A: Many DSCR Lenders offer cash-out refinancing, allowing you to access up to 75.0% of your rental property’s equity, without verifying personal income. However, DSCR cash-out loans are strictly for rental properties (business purpose). Proceeds also cannot be used for personal expenses like income taxes, credit card debt, or student loans. DSCR Lenders typically require a written statement (on the application) or signed disclosure letter confirming the intended business use of funds, which can (and typically are) used for further real estate investing.

Since most DSCR Loans have borrowers that are entities such as LLCs, most DSCR Loan applications will have a separate section for entity details if it’s applicable. While all of the entity docs will be collected later on and information verified and checked, the crucial reason for entity information at the application stage is the names and ownership percentages of each individual owner of the entity since this will determine who is required to be a guarantor on the loan. Requirements can vary among lenders for what the ownership threshold of an entity is to require a personal guaranty (typically around 25%). But this is the stage of the process where the credit reports are run, so understanding the ownership splits and for whom the lender needs to get credit authorization and credit reports is determined from this section.

Q: Do I have to personally guarantee a DSCR loan if I use an LLC?

A: Yes, in most cases. Even if the DSCR loan is made in the name of an LLC or other business entity, lenders require a personal guarantee from any borrower or owner with a significant ownership stake, typically each individual with 25% or more ownership and at least 50% of aggregate total ownership.

The final aspect of a DSCR Loan application will likely include a borrower personal information section and then a series of “Declarations” around potential credit or personal issues that might have a serious impact on the ability to pay back the loan.

The personal information section will likely have questions such as: full name, date of birth, marital status, home address, Social Security number and contact information like phone number and e-mail address for each guarantor of the loan. These questions serve multiple purposes, mainly around ensuring that credit reports, fraud and background checks and other lender due diligence can be done correctly. These questions are normal and necessary for the lender to fully process a DSCR Loan application.

Next will likely come a Borrower Demographic Information section where you will be asked information related to sex, ethnicity and race. Note that while conventional lenders and lenders offering loans for intended owner-occupants are legally required to do so, it is a grey area on whether or not it is truly required by DSCR Lenders. Regardless, this section is always optional for each borrower (guarantor) and there should always be a “Do not wish to provide” box for each demographic question.

Finally, there is a series of Declarations that each guarantor must answer honestly and sign accordingly, meaning any dishonesty here is a significant issue and would constitute a form of mortgage fraud that could have serious consequences. While most DSCR Lenders will seek information on these areas through credit reports, background checks and other forms of financial underwriting, some information may not be found there or otherwise slip through the cracks. These attestations are an important part of the application and should always be answered fully and transparently.

These are all formatted as “Yes/No” questions and a letter of explanation attached to the application, or at least further details will likely be required for each “Yes” answer (the sole exception is the “Are you a U.S. citizen?” question).

In addition to the application, a DSCR lender will ask for what’s commonly referred to as a Credit Authorization so that they can run a full “hard” credit report for each potential guarantor. Because running this report requires personal information (including Social Security numbers) and generates personal information (as well as the potential negative impact to credit for each inquiry), the lender must have signed consent to run the report. This document can typically also be signed electronically and is often integrated within the application.

Q: What documents are required for a DSCR loan application?

A: Since DSCR Loans don’t require income verification or use a DTI Ratio, there is little documentation required to fully complete a loan application, typically all that is needed is to fill out and sign a short form and giving the lender authorization to run a credit and background report. It’s typically a 15-minute exercise, and the required documents, like leases or LLC entity docs, are only required later in the process once the application has been approved.

Up Next: If you qualify and the credit report checks out, you are ready for the next stage where you'll receive a "Term Sheet" or "Letter of Intent (LOI)" from the lender with initial terms and potentially a rate lock.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.