.png)

Now that we’ve reviewed how DSCR Lenders determine base rate stacks and apply LLPAs across credit, leverage, cash flow, and other risk metrics, it’s time to see how everything comes together in practice. Let’s walk through a real-world example of pricing, generating five different loan quote options using the same borrower and deal profile. We’ll explore how small changes to the structure, such as adjusting the LTV or prepayment penalty, affect the interest rate, premium, and closing points.

As you can probably see by this point, “What are the current DSCR loan interest rates?” while a common question, doesn’t really have an answer. DSCR Loan rates are generated through a combination of many factors including both the base rate stack (connected to market rates) and a whole host of LLPAs based on borrower and property specifics, so there is no real current “DSCR Loan Interest Rate.”

However, one way to at least partially answer the question is to look at representative scenarios, or a generic example of what a common loan may look like. This allows a general picture of what DSCR Loan interest rates may look like, and how that answer can change not only thorough time as market rates go up and down, but also how investors and lenders can work together to tailor loan terms to their preferences (low rates versus low points, different leverages, etc.).

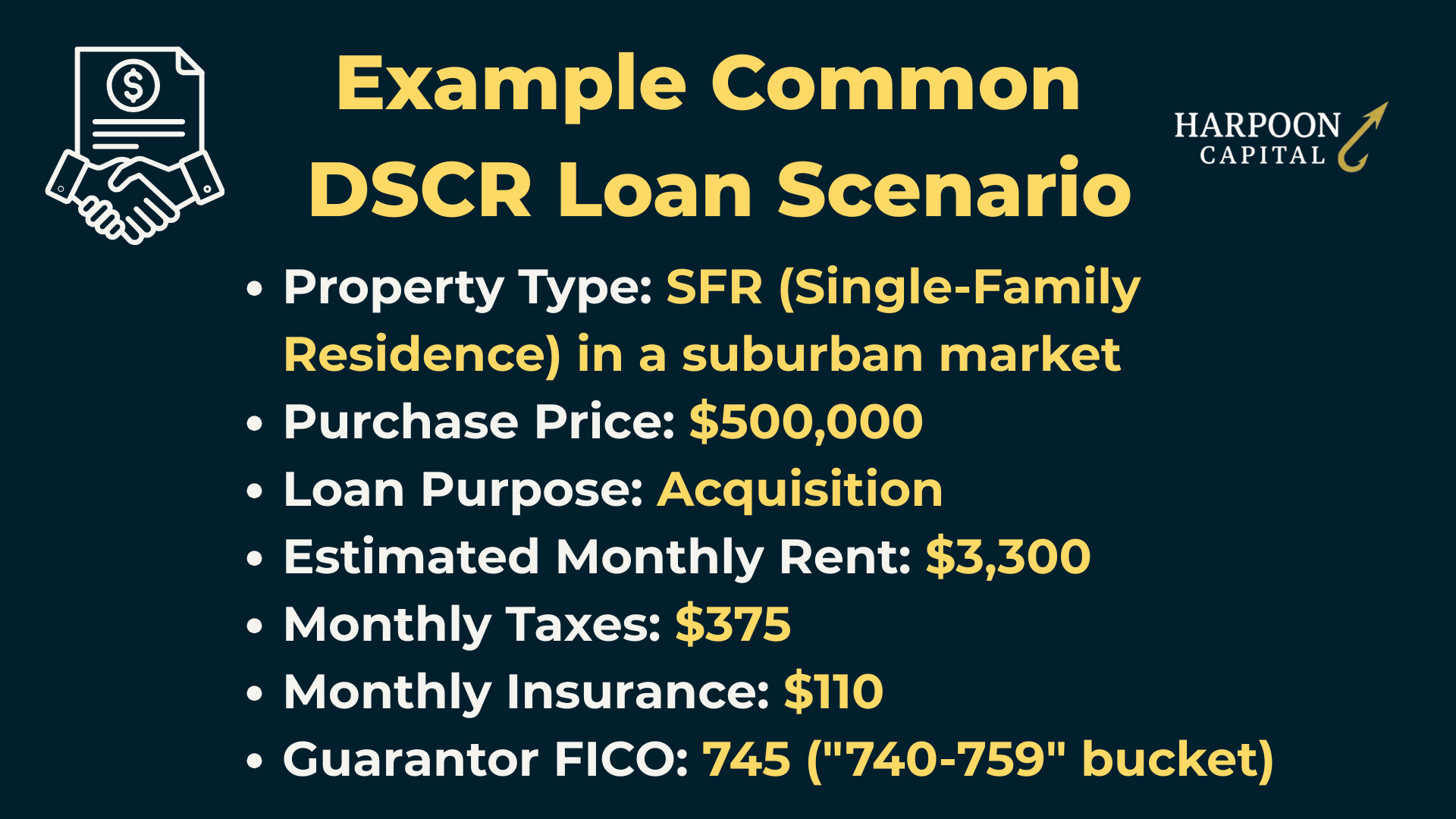

The following represents a common scenario where a real estate investor is looking to purchase a Single-Family Residence (SFR) in a non-rural market at typical price point of $500,000 for a traditional buy-and-hold investing strategy. The investor wants to minimize down payment and do maximum leverage (20% down, 80% LTV) but wants to see what their options might look like if they put more down (such as 25% or 30%). They are investing through an LLC (so borrower will be that entity) but own 100% of the entity and will be the sole guarantor, and their credit report shows a good score of 745, with no credit issues, a clean report showing no recent mortgage lates or credit events. This places them in the 740-759 FICO bucket, not quite the best, but up there. The investor estimates the monthly market rent to be $3,300 with monthly property taxes of $375 and monthly property insurance of $110.

We’ll now walk through five pricing structures a DSCR Lender may quote based on this scenario. Each quote uses a different LTV or prepayment structure, with the base rate selected from the rate stack and adjusted using LLPAs per the matrices covered in Step 2. Importantly, for this example, the DSCR Lender has a pricing policy that aims to achieve a net 102.5 price (sum of premium and closing fee). This indicates a 2.5% gross margin (or lender profit margin before taking into account operating costs like employee labor, office rents, marketing, etc.). The way this generally works is to first find the loan premium and then the difference must be made up from closing fee. For example, if the loan premium is at par (i.e. “100”), then the entire profit margin or 2.5%, must be made up for in closing fee (2.5%).

The first quote shows what the loan pricing would look like for a DSCR Loan if the borrower wanted to do the typical “max LTV” by minimizing the down payment, in this case putting 20% down (or $100,000 on the $500,000 property). This scenario also shows a standard fixed rate loan structure that’s fully amortizing, with the typical 5/4/3/2/1 prepayment structure found on most DSCR Loans.

DSCR Loan Terms:

DSCR Ratio Calculation:

DSCR: $39,600 ÷ $37,752 = 1.05x

DSCR Loan Interest Rate & Premium Computation:

LLPA Adjustments:

Adjusted Premium: 99.750 + 0.250 = 100.000

Closing Fee: 102.500 (pricing “hurdle”) – 100.00 (adjusted premium) = 2.5 (Closing Fee)

DSCR Loan Interest Rate & Closing Fee Generated:

Key Takeaways:

This is a classic high-leverage standard scenario. The borrower pushes to the 80.0% LTV ceiling, which causes a 37.5 basis point negative LLPA adjustment despite the good credit score. The borrower is still able to maintain an interest rate of just 7.000% which is towards the lower end of the lender’s rate range (6.5% - 8.5%), but since the adjusted premium is par or “100,” they have to cover the lender’s entire needed margin through the closing fee, which is hefty but a not overwhelming two-and-a-half points. The DSCR ratio is 1.05x, thin, but in positive territory, providing cash flow and avoiding the sub-1.00x DSCR buckets that come with additional and significant negative LLPAs and restrictions.

In the second scenario, we will see how the borrower can lower interest rate and improve cash flow (increase DSCR ratio from 1.05x to 1.13x) while paying the same number of points. Through a slightly increased down payment (from 20% to 25%, or an additional $25,000) and upping the prepayment penalty to a 5/5/5/5/5 (or “5%(60),O(300)”) structure vs. 5/4/3/2/1 (not a huge issue for this buyer aiming for a long-term buy and hold cash flow strategy), they are able to lower their rate from 7.000% down to 6.750%.

DSCR Loan Terms:

DSCR Ratio Calculation:

DSCR: $39,600 ÷ $35,004 = 1.13x

DSCR Loan Interest Rate & Premium Computation:

LLPA Adjustments:

Adjusted Premium: 99.750 + 0.250 = 100.000

Closing Fee: 102.500 (pricing “hurdle”) – 100.00 (adjusted premium) = 2.5 (Closing Fee)

DSCR Loan Interest Rate & Closing Fee Generated:

Key Takeaways:

Reducing leverage even by just 5% improves pricing quite a bit. The borrower still falls into the same DSCR bucket, but the improved rate and bigger down payment saves roughly $230 per month, which is quite significant for a deal this size. The heavier prepay structure is what makes this lower rate viable at par pricing. One note here is that while it may seem like the borrower should further tweak the terms to get into the next DSCR bucket starting at 1.15x, per the matrix that wouldn’t actually affect pricing at this LTV. While this isn’t universal among lenders, it’s illustrative in how many DSCR lenders treat minor LTV ratio changes much more significantly than minor differences in DSCR ratio.

For the next option, we’ll see what it looks like if the borrower is willing to stomach a higher rate even at the reduced leverage (25% down), but wants to cut down on the closing points. By upping the interest rate to 7.500%, the borrower can still maintain cash flow (positive DSCR ratio), while reducing the closing fee significantly, down from 2.5 points to 0.75 points, an upfront savings of over $6,500!

DSCR Loan Terms:

DSCR Ratio Calculation:

DSCR: $39,600 ÷ $37,296 = 1.06x

DSCR Loan Interest Rate & Premium Computation:

LLPA Adjustments:

Adjusted Premium: 100.750 + 1.000 = 101.750

Closing Fee: 102.500 (pricing “hurdle”) – 101.750 (adjusted premium) = 0.750 (Closing Fee)

DSCR Loan Interest Rate & Closing Fee Generated:

Key Takeaways:

While the higher interest rate kicks up the monthly payment and reduced the DSCR ratio back down to 1.06x (even at the lower leverage point), the upfront savings (2.5 points to 0.75 points or $9,375 to $2,812.50) is very significant and an attractive option to a lot of investors, especially those that like to move money around and do lots of deals where plunking down almost $10,000 in closing fees on a deal like this isn’t ideal. Comparing this option to scenario 2 (with much lower rate and 2.5% closing fee) really comes down to time horizon too – the monthly payment difference of $191 will only eclipse the savings of $6,562.50 in 35 months or approximately three years, which is another good way for investors to think about pricing options when comparing quotes, especially when thinking how long the investment plan is for.

This option looks at what might be available if the borrower drops the leverage point even further, to a full 30% down payment, for a 70.0% LTV. It also shows what is called “par” pricing where there is zero closing fee. While the investor is now having to put down a full $150,000 down payment (another $25,000 vs. the 75.0% LTV options), at the end of the day that money is still equity owned by the borrower, in this scenario it is just now invested in the property. Closing fees are expenses and money spent with zero closing fee and a larger down payment, more money (or really value) is retained by the investor.

DSCR Loan Terms:

DSCR Ratio Calculation:

DSCR: $39,600 ÷ $35,976 = 1.10x

DSCR Loan Interest Rate & Premium Computation:

LLPA Adjustments:

Adjusted Premium: 100.750 + 1.000 = 102.500

Closing Fee: 102.500 (pricing “hurdle”) – 102.500 (adjusted premium) = 0.000 (Closing Fee)

DSCR Loan Interest Rate & Closing Fee Generated:

Key Takeaways:

With the reduction in LTV, the borrower gets a boost in monthly cash flow despite the higher interest rate since the loan amount is lower and gaining an additional LLPA boost from the lower LTV bucket. This structure, with a 1.10x DSCR ratio and no closing fee can be attractive to a lot of investors regardless of strategy – Par pricing or zero point pricing is pretty popular!

A final option looks at what a DSCR Loan with zero prepayment penalty options might look like, moving back to a more typical (for DSCR Loans) down payment of 25% for a 75.0% LTV. Immediately noticeable is the gigantic jump in rate that this scenario entails, up to 8.500%, or the highest option available from this lender – without the corresponding reduction in closing fee – still 2 points upfront. Prepayment flexibility – in this case, ability to prepay whenever with zero fee – has quite a cost!

DSCR Loan Terms:

DSCR Ratio Calculation:

DSCR: $39,600 ÷ $37,692 = 1.05x

DSCR Loan Interest Rate & Premium Computation:

LLPA Adjustments:

Adjusted Premium: 102.500 - 2.000 = 100.500

Closing Fee: 102.500 (pricing “hurdle”) – 100.500 (adjusted premium) = 2.0 (Closing Fee)

DSCR Loan Interest Rate & Closing Fee Generated:

Key Takeaways:

The key takeaway for this scenario is the illustration of just how much prepayment penalties improve pricing on DSCR Loans and are a key aspect of what can make them competitive with conventional financing options. Here, the investor has to pay a much higher rate and significant closing fees and still has pull multiple levers – Partial-IO and Hybrid (Fixed to ARM) structure just to get small cash flow (1.05x DSCR ratio). This type of structure can work well for some investors, especially those that like to buy and sell frequently or want to gamble on market rates lowering soon, however it comes with quite a price tag. This scenario, especially when compared with the prior scenarios with more standard five-year prepays, shows the folly of state regulations that ban or restrict prepayment penalty provisions for DSCR Loans. Rather than “helping” investors like they are ostensibly intended to do, they do the opposite, limiting investors in those states to high rates and fees and much reduced flexibility!

DSCR Loan pricing is not just a formula, it’s a multi-variable negotiation. While base interest rates are grounded in market factors outside both lender and borrower control, the rates received is shaped by multiple risk factors and loan levers that work together to set the terms.

From FICO and LTV to property type, loan size and especially prepayment penalties, each adjustment represents how DSCR Lenders perceive and price “risk” to generate the needed “reward”. When layered together, these adjustments create significant variability in interest rates and fees. As seen in the examples, two loan quotes with the same property and borrower could vary by over 150 basis points in rate or thousands of dollars in fees just by changing structural features or balance of upfront cost versus spreading it out over the term.

The key insight? Investors (DSCR Loan borrowers) have far more control over DSCR Loan terms than might be expected. Ultimately, pricing is dynamic, but the logic behind it is learnable. With the tools in this section, you now have the knowledge to go beyond just rate-shopping, and instead understand exactly how the “DSCR sausage” gets made and how to construct the ideal financing structure and strategy for your deals.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.