.png)

When most people picture a traditional DSCR Loan, they think of a one-to-four-unit property occupied by individual tenants under individual leases for each unit, often referred to as long-term rentals or “LTR.” In this classic scenario, the lease is a key document utilized to evaluate the rental revenue of the property, or the numerator in the critical debt-service-coverage-ratio.

However, as DSCR lending has expanded, so have the property types and investment strategies it supports. Many investors now use DSCR Loans to acquire vacant or mismanaged properties for repositioning, or to operate short-term and medium-term rentals where revenue may be documented via actual booking history or via market-based projections (e.g., AirDNA or other lender-accepted market rent analyses) when limited or no operating history exists.

Because of this variety, leases are not a universal requirement in DSCR lending. They are considered conditional documentation, only required when the property is occupied by long-term tenants and there’s an active lease in place.

While there are multiple rules and factors used by DSCR Lenders to underwrite rent (i.e. to choose the number to use in the numerator of the DSCR ratio calculation), an actual, in-place lease agreement is one of the most concrete pieces of evidence available to support an underwritten rent expectation. Similar to how “value” is determined, the most trusted market value figures are often from real acquisitions, where an actual buyer and seller have agreed to a price, rather than from refinances relying solely on an appraisal estimate. The same logic applies to revenue: market rents are always just an informed guess, but a valid lease, even if slightly above or below market, provides tangible proof that a tenant has agreed to pay a specific rent amount under enforceable terms.

Q: What is proof of collections in a DSCR Loan, and when is it required?

A: Proof of collections is documentation, such as bank statements, payment ledgers, or canceled checks, showing that tenants have actually paid the rent stated in the lease. A minority of DSCR Lenders require this routinely, while others only ask for it when lease rents are far above market or when they want to confirm the tenancy is real and performing.

While leases are a straightforward and familiar document to most investors, DSCR Lenders have several important requirements for the specific lease documents. These requirements can frequently require revisions and back and forth that can hinder or delay the DSCR Loan process. While some of these requirements can seem nitpicky and draconian, it’s important to remember that DSCR Lenders can often be the target of mortgage fraud, especially occupancy fraud (i.e. fake or fraudulent leases) and unfortunately, lease agreements can be doctored more easily than other document types (such as compared to reports from financial institutions or third party appraisals that must go through AMCs and other safeguards). Because of the relative ease of fraud around leases and occupancy, and the unfortunate example being set by prominent societal leaders like New York Attorney General Letitia James and Federal Reserve member Lisa Cook, DSCR Lenders are always on alert for fake or altered leases, and the documentation requirements for leases are thus fairly strict and detailed.

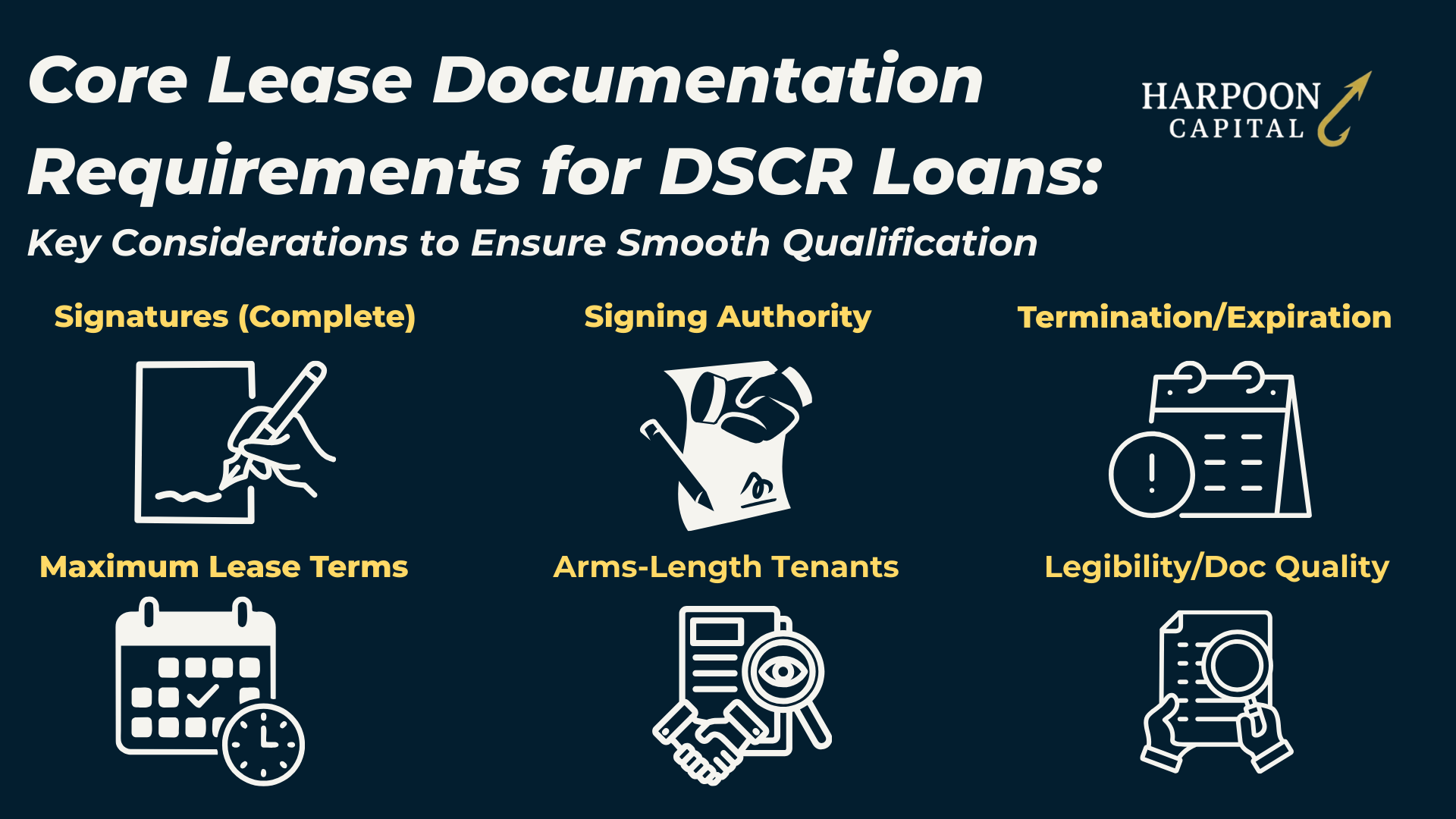

While the exact checklist can vary by lender, most DSCR needs lists will require leases to meet standards around signatures, terms and provisions around termination and expirations. Additionally, many DSCR Lenders will have hurdles around lease legibility as well as anti-fraud measures around confirming authenticity and arms-length nature of tenancy.

When it comes to lease signature and execution requirements, it’s typically required that there are full and complete signatures (including dates) by both parties, including the tenant and the landlord. While a property manager may also be authorized to sign, documentation of such agreement would likely be needed if that is the case. Additionally, many leases likely require tenant initials on each page, or throughout the lease document, and most lenders will require these to not be missed or skipped. Finally, an additional consideration is that sometimes leases may be signed by the guarantor (i.e. individual person), but the property is vested to an entity, like an LLC. In these cases, the DSCR Lender may require that the lease would be signed by the true entity owner rather than the individual, even in cases where that individual owns 100% of the entity. How strict a DSCR Lender will be about all of these seemingly minor items (i.e. missing initials, individual vs. LLC signature block, etc.) will vary from lender to lender, it’s typically in the interest of both borrower and lender that these items are fully buttoned up and correct, as there is a national trend and very real risk of incurring costs, headaches or other significant troubles with tenants utilizing the court system to challenge and frustrate property owners, and can grasp on the smallest items to cause significant financial loss.

It’s important to note that the signature for the landlord should match signing authority according to the entity documentation (if the borrower is an entity like an LLC). A common pitfall that adds delays and complications to the DSCR Loan process is instances where someone had signed the lease (as landlord) that wasn’t part of the entity and had no signing authority, requiring reworking of the documents.

Lease terms and provisions around termination or lease expiration are also an important aspect of lease documentation analysis for DSCR Loans. Generally, leases for properties securing DSCR Loans just need to not be expired at closing date. If the expiration date of the lease is past the date of loan closing, the lease should be fine. Additionally, leases that are month-to-month are also okay for DSCR Loans, and particularly, leases that are expired but include language that says the lease reverts to month-to-month (“MTM”) post-expiration (typically with both parties, tenant and landlord holding the right to terminate any time), are also okay for DSCR Lenders. However, if a lease is expired but doesn’t include that relatively common “reverts to MTM post-expiration,” such lease will not be acceptable. As such, even if a lease is due to still be in effect through the planned closing date, due to the frequency of DSCR Loan deal delays and “pushes,” it’s smart to make sure leases are either proactively renewed or include this post-expiration MTM language specifically if any expirations are within a month or two of planned closing.

Additionally, a little-known aspect of lease requirements for DSCR Loans is there are often maximum lease terms for tenancy. Typically, most DSCR Lenders will allow leases of only up to two or three year original terms, with anything longer not eligible. While reasons for this can vary, it’s likely because lenders want to avoid situations where the landlord is prevented from raising rents in a rising-rent market environment but also because greater than one-year leases are unusual for residential rentals, and can indicate a non-permitted use or other fraud flags.

A key consideration for DSCR Lenders around lease documentation is confirming arm’s length tenancy, i.e. that the tenant is unrelated to the landlord (i.e. borrower), and the lease agreement and rents represent legitimate market transactions. Non-Arm’s Length leases provide multiple potential problems for lenders. One, it is a sign and common method of potential occupancy mortgage fraud, as it could be an instance of the borrower utilizing what is supposed to be a rental property to house family or themselves (while having a trusted family member fake living there).

Additionally, with many DSCR Lenders enacting more borrower-friendly underwriting of revenue for above-market leases, such as allowing in-place rents to be used to qualify the rental revenue in the DSCR ratio when they are higher than market rent, this unfortunately invites dishonest borrowers to fake leases to show above-market rent needed to qualify. Finally, even if the leases are above board and represent an honest market rent relationship where the property happens to be leased out to a family member, there is generalized higher risk for landlords to be more lenient with tenants who are related when missed payments or trouble arises. This results in a less durable DSCR ratio and ability for the property to make PITIA payments. Overall, while it is hard for a DSCR Lender to always detect, a significant part of DSCR Loan lease documentation review will be a close look to confirm the leasing relationship is at arm’s-length, past the more perfunctory signature and expiration date checks.

Finally, one of the most frequent problems with lease documentation for DSCR Loan is simply poor legibility and documentation quality for the leases provided. An unfortunate but common occurrence in real estate lending is poor file organization, especially around leases, where the document files are sloppily scanned and/or poorly named and labeled (or missing pages). It’s common for there to be multiple lease amendments as well, which provide further opportunities for missing documents (i.e. missing the original lease or one of the amendments) or poor labeling (unclear how many amendments have been made, which units tie to which leases, etc.). It is definitely one of the best borrower practices for DSCR Loans to take the extra time and effort to organize and properly scan and label leases before providing them to the lender. This will almost certainly significantly increase the speed of processing the DSCR Loan and be highly appreciated by the lender’s operations team, putting a file on top priority and on track for a smooth close.

Q: What are the most common lease-related mistakes that delay DSCR Loan closings?

A: The most frequent errors include missing signatures, non-arm’s-length tenants, expiring leases with no MTM clause, illegible scans and overly long lease terms. Additionally, if there are any changes to the original lease agreement that have been crossed off and new terms written in, a failure for each change to be properly initialed by both parties is common, requiring an update.

While most DSCR Lenders will be satisfied using the lease alone, a more conservative segment of the market, roughly one-quarter to one-third of active DSCR Lenders, require proof of actual rent collections as part of the lease documentation. This typically means providing two or more months of evidence showing the tenant has paid as agreed, such as: bank statements showing rent deposits, payment ledgers from a property management system or canceled checks or electronic payment confirmations.

The purpose is to ensure the lease is not simply “on paper” but reflects a real, performing tenancy. Unfortunately, falsified leases are a known form of mortgage fraud, sometimes used to inflate property revenue for qualification. In other cases, the lease exists but the tenant actually pays a different amount “under the table” than what’s stated in the agreement.

From the DSCR Lender’s perspective, proof of collections strengthens underwriting by verifying that the rent stated in the lease is both real and collectible. However, many DSCR Lenders do not require this in order to remain more competitive, since it adds to the borrower’s paperwork burden and can slow the process. As long as the lease terms and rent amounts are at or near market rent levels, many lenders are comfortable relying on the lease alone.

Some DSCR Lenders take a hybrid approach to proof of collections, requiring proof of collections only in cases where the lease rent is significantly higher than the appraisal-determined market rent or in cases where the lease has expired and converted to a mutually-terminable month-to-month arrangement. Additionally, the more sophisticated DSCR Lenders will likely review the borrower’s (guarantor’s) background report to see if the tenant and the sponsor were “known associates,” especially in cases for brand new leases and higher-than-market rent. In these situations, the higher-than-market rent may trigger a deeper review to rule out fraud or to understand if an unusual arrangement is in place with a particular tenant or property.

Q: Do DSCR Lenders require proof of rent payments in addition to the lease?

A: Some DSCR Lenders, usually more conservative lenders or when the in-place lease rent is well above market, will require recent proof of rental collections to confirm the lease is real and performing. Many others skip this step to keep the process faster and with less paperwork, as long as lease terms appear reasonable and at or near market rent.

Up Next: Find out the documentation requirements when your property is a short term rental with operating history but no leases.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.