.png)

Most DSCR Lenders, even those that don’t market themselves as “STR-friendly,” will allow short-term rental–based qualification on refinances if there are at least 12 consecutive months of the property’s operation as a short-term rental. The “12 months” in this context means providing TTM Actuals (i.e. the actual revenue for the trailing twelve months). This generally refers to a backward-looking 12-month period, typically starting with the month prior to the closing month of the new DSCR Loan.

For example, if a DSCR Loan closes in August 2025, the TTM period would be August 2024 through July 2025. The count is strictly historical; future bookings or in-progress stays generally cannot be counted toward the TTM total. Additionally, actual lender policy on when the “TTM Actuals” lookback period starts, i.e. from the closing date, month prior to the closing date, or even application date, can vary, and be complicated by shifting timelines, frequent in DSCR Loan cycles. Investors looking to refinance short term rental properties with an operating history should confirm the specific TTM Actuals period rules from the DSCR Lender early in the process so there are no surprises or unnecessary delays.

TTM Actuals documentation is generally not allowed for acquisition DSCR loans when the 12-month history belongs to the seller, not the borrower. In rare cases, a small number of DSCR Lenders, or a DSCR Lender making a case-by-case exception, may allow the seller’s TTM Actuals to qualify, such as if the borrower is keeping the same property manager, already has STR experience in the market or can provide additional supporting documentation. These scenarios are the exception, not the rule, so borrowers should not count on this being approved.

Q: What does TTM mean in DSCR loans?

A: In DSCR lending, TTM stands for Trailing Twelve Months and refers to the most recent 12 full months of actual property performance, ending with the month before the loan closing date. For example, if you apply in February 2025, your TTM period would be February 2024 through January 2025.

DSCR Lenders require clear, verifiable, and directly sourced documentation that ties to the subject property when “TTM Actuals” are utilized as documentation for rental revenue on a short term rental refinance. This documentation most commonly requires revenue history downloaded directly from an official booking platform (i.e. airbnb, VRBO) or generated as a signed report from a property manager if a separate booking/accounting system is used. Alternatively, Platform Payout Summaries, showing gross monthly revenue for the past 12 months, either via platform-generated reports or borrower bank statements could also typically be used.

It’s also important to note that DSCR Lenders usually base the qualifying revenue on gross booking revenue for the rooms/units only, and exclude cleaning fees, pet fees, resort fees, or other non-room charges are excluded and they will not typically deduct management fees, taxes, or operating expenses, even if these costs are included in the provided operating history. DSCR Lenders will usually use the gross rental figure as the basis for DSCR ratio calculations, which is a major reason why DSCR Loans are often preferred by STR investors, as this revenue methodology is very borrower-friendly.

While providing TTM Actuals documentation for long-running STRs is fairly straightforward, there are a couple of additional nuances to be on the lookout for. One common pitfall is related to counting future or in-progress bookings, as many short-term rentals have calendars booked a couple of months ahead. While many platforms may have non-refundable policies and revenue from these stays may be very likely locked in, most DSCR Lenders will not allow future or even in-progress (stay in progress at closing date) to count towards TTM Actuals documentation. While there may be some room along the edges for exceptions, maybe around an in-progress stay or something similar, typically trailing twelve months means trailing only and if revenue is needed from future stays to qualify, planning a later closing date may be the best, and only option. Additionally, the DSCR Lender may require a simple screenshot or link to the property listing to verify the property’s history is really for such property, but this should be a very quick and easy documentation task for any legitimate investor. The property may appear in airbnb bookings documentation as the name of the listing (such as “Cozy Cottage at the Beach”) and not show the property address, so the additional documentation confirming the revenue is indeed associated with the property under review is critical.

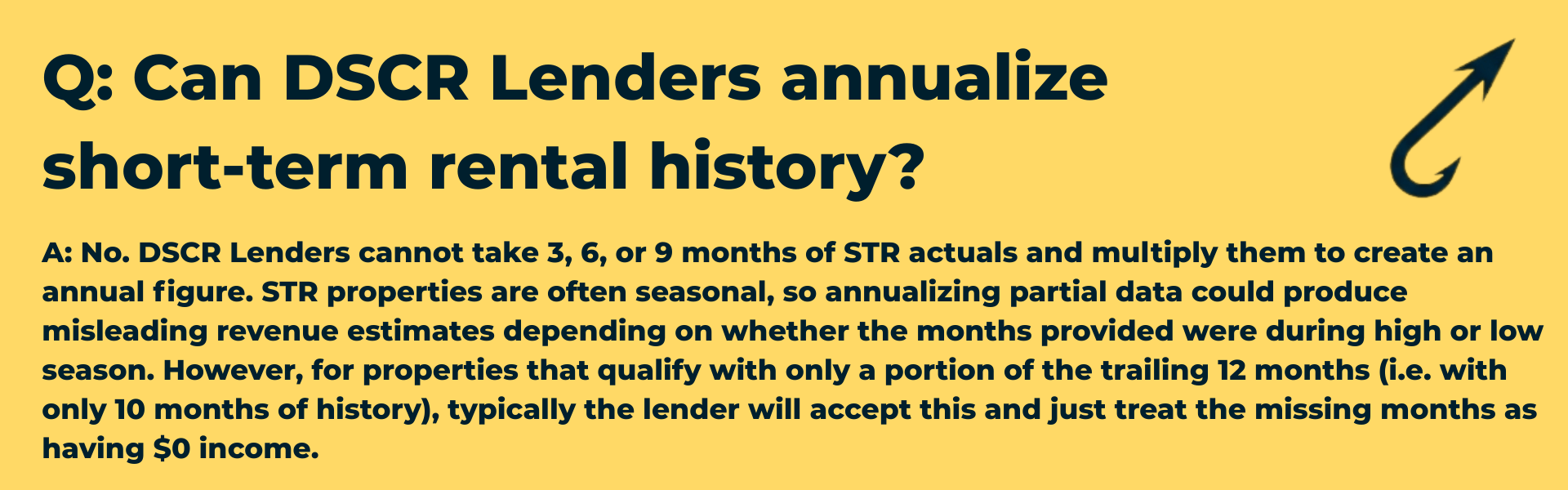

Q: Can DSCR Lenders annualize short-term rental history?

A: No. DSCR Lenders cannot take 3, 6, or 9 months of STR actuals and multiply them to create an annual figure. STR properties are often seasonal, so annualizing partial data could produce misleading revenue estimates depending on whether the months provided were during high or low season. However, for properties that qualify with only a portion of the trailing 12 months (i.e. with only 10 months of history), typically the lender will accept this and just treat the missing months as having $0 income.

Up Next: Learn about all the needed Purchase Contract Documentation for DSCR Loans used for property acquisitions!

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.