.png)

Referral Rules and Licensing Rules (for acting as a “Mortgage Broker) for DSCR loans break down similarly to that of prepayment penalties – most states have no restrictions, meaning anyone can refer DSCR Loans, including with no limits on referral fees or compensation! However, like prepayment penalty provision rules, there are a handful of states that have specific regulations related to brokering mortgage loans, meaning anyone “arranging” rental property financing, including professional mortgage brokers, must have specified licenses for the state through the NMLS (Nationwide Mortgage Licensing System), similar to the regulations around brokering conventional or other consumer loans. Finally, there are a couple states with “vague” laws that some more conservative lenders may interpret as needing a license, but it’s not clear cut, and lenders can differ in policy.

As with many aspects of our legal and regulatory system, these laws and rules can significantly lag behind changes in technology and society, i.e. laws written in the 1990s for example couldn’t have anticipated people building large referral networks through facebook and Instagram and monetizing mortgage loan referrals the same way their peers might hawk digital products or skincare lotions. While some state regulations may appear misguided or outdated, remember it takes a while for many state legislatures to get with the times, and it’s likely these will get updated or attain more clarified interpretations in the near future.

These states have no restrictions or licensing requirements to refer DSCR Loans: Alabama, Arkansas, Colorado, Connecticut, DC, Florida, Georgia, Hawaii, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Massachusetts, Missouri, Montana, Nebraska, New Hampshire, New York, North Carolina, Ohio, Oklahoma, Pennsylvania, Rhode Island, South Carolina, Tennessee, Texas, Vermont, Washington, West Virginia, Wisconsin, Wyoming. For investment properties in these states, anyone can refer DSCR Loans and receive referral fees or compensation for the referral or freely earn a commission on the closed loan (i.e. 0.50% of the loan amount dependent on close).

The following states have restrictions or prohibitions on referring or brokering DSCR Loans without required licensing, typically through the NMLS and related to official mortgage brokering. Ironically, most of these states are in the western region of the United States, the opposite of the “Wild West” stereotype of looser regulations within states on the left side of the map. These states include Arizona, California, Idaho, Nevada, Oregon, Utah, North Dakota and South Dakota.

The following is a breakdown of state-specific rules on referral fees prospective DSCR Loan referrers - professional mortgage broker or “regular person” - should watch out for.

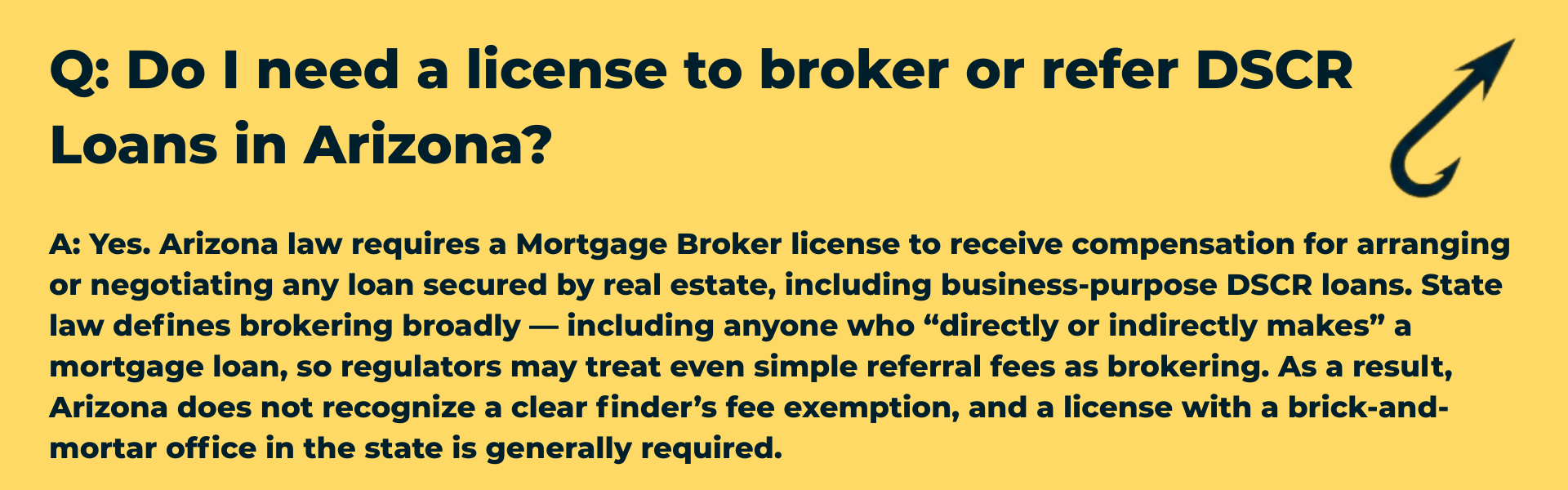

For Arizona, the state regulations (A.R.S. § 6-903) state that “A person shall not act as a mortgage broker if the person is not licensed” and “person is not entitled to receive compensation in connection with arranging for or negotiating a mortgage loan if such person is not licensed” (A.R.S. § 6-909). Mortgage Loans are defined as “a loan secured by a mortgage or deed of trust or any lien interest on real estate located in this state created with the consent of the owner of the real estate” and there is no ambiguity between residential and commercial, or residential business-purpose or consumer. As such, it’s clear that anyone seeking to refer mortgage loans, including DSCR Loans, in Arizona must have the proper licensing from the NMLS and the state. Note that “brokering” is broadly defined as anyone who “for compensation or in the expectation of compensation either directly or indirectly makes, negotiates or offers to make or negotiate a mortgage loan” so the “indirectly makes” language can likely be interpreted multiple different ways, and can arguably even include simple introductions to lenders in exchange for a referral fee, while could also by some be viewed as okay as long as the referrer doesn’t participate in any “negotiations.”

Q: Do I need a license to broker or refer DSCR Loans in Arizona?

A: Yes. Arizona law requires a Mortgage Broker license to receive compensation for arranging or negotiating any loan secured by real estate, including business-purpose DSCR loans. State law defines brokering broadly — including anyone who “directly or indirectly makes” a mortgage loan, so regulators may treat even simple referral fees as brokering. As a result, Arizona does not recognize a clear finder’s fee exemption, and a license with a brick-and-mortar office in the state is generally required.

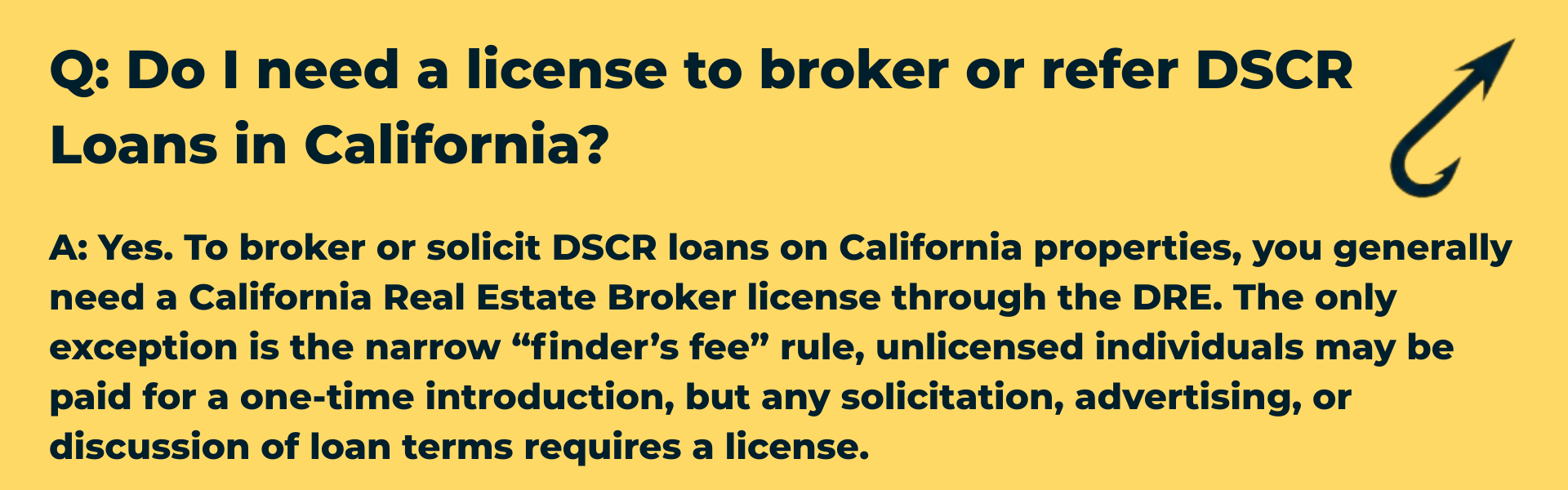

California’s “California Financing Law (CFL)” applies the state’s famously extensive regulations to the lending industry, with mortgage loans included. Additionally, California is unique in that its “real estate broker” laws group the need for a license to arrange loans for real estate, with the licensing requirements for real estate brokers (agents) working in buying and selling real estate, as well as leasing. The CA Bus & Prof Code § 10131 (2024) defines “real estate broker” to include anyone who “solicits borrowers or lenders for or negotiates loans or collects payments or performs services for borrowers or lenders or note owners in connection with loans secured directly or collaterally by liens on real property.” California tends to not differentiate between DSCR Loans and other consumer-based mortgage loans for these purposes, so having a California Real Estate Broker License through the DRE appears to be a requirement to broker or refer DSCR Loans in the Golden State.

However, there is a key “carve-out” for California around a defined “finder’s fee” exemption where if the referrer does not solicit and only makes an introduction then “a referral fee to an unlicensed individual—but only if that person does not solicit clients or participate in the transaction beyond making the introduction.” The legal analysis is extensive, but it generally appears that there is a consensus that as long as it’s truly limited to a “finder’s fee” and that the referrer never “crosses into negotiation or communication between the parties” past the intro, then referring and collecting compensation is okay. This is somewhat ironic since the interpretation appears to make it okay for an individual not in the mortgage industry to be able to collect referral compensation for referring a DSCR Loan, but a professional mortgage broker that’s licensed in another state (for example, being NMLS-licensed in Texas only) would run afoul of being able to broker DSCR Loans in California if he or she solicits mortgage clients or plays any role in negotiating or explaining loan parameters!

In summary: referral fees for DSCR Loans in California are allowed, but allowed under the strict “finder’s fee” exemption – just an introduction and no active soliciting for referrals allowed.

Q: Do I need a license to broker or refer DSCR Loans in California?

A: Yes. To broker or solicit DSCR loans on California properties, you generally need a California Real Estate Broker license through the DRE. The only exception is the narrow “finder’s fee” rule, unlicensed individuals may be paid for a one-time introduction, but any solicitation, advertising, or discussion of loan terms requires a license.

For Idaho, the state has fairly clear definitions when it comes to “residential mortgage loans” and “mortgage brokering activities” related to these loans. Idaho defines “residential mortgage loan” as “any loan that is secured by a mortgage, deed of trust, or other equivalent consensual security interest on a dwelling...or on residential real estate” and doesn’t make a distinction between owner-occupied or business-purpose residential real estate. Additionally, it has relatively clear definitions related to “mortgage brokering activities” which it defines as “for compensation or gain or in the expectation of compensation or gain, either directly or indirectly, accepting or offering to accept an application for a residential mortgage loan, assisting or offering to assist in the preparation of an application for a residential mortgage loan on behalf of a borrower, negotiating or offering to negotiate the terms or conditions of a residential mortgage loan with any person making residential mortgage loans, or engaging in loan modification activities on behalf of a borrower.” And to tie it together, the state of Idaho requires a state license to engage in mortgage brokering activities without a license from the state (ID Code § 26-31-203). The applicable department for the required licensing is the Idaho Department of Finance that works through the NMLS.

With regards to allowing referral fees, Idaho is another example of a somewhat vague line between simple “finders fees” and hands-off referrals and actual “brokering activities” where it could be reasonably interpreted that just referring a borrower for a referral fee, without playing any role in the process, including the initial application, should be okay, but any true performance as a mortgage broker would not be allowed. Additionally, there does not appear to be explicit prohibitory language against “soliciting” without a license, so there may be more room to maneuver for promoting DSCR Loans, for example among social media followers in Idaho than say, California, where solicitation is more explicitly prohibited.

Q: Do I need a license to broker or refer DSCR Loans in Idaho?

A: Yes. Idaho law requires a state Mortgage Broker license (through NMLS) to receive compensation for “brokering activities” for “residential mortgage loans” in the state, which include DSCR Loans. However, the regulations have a fairly robust definition of “brokering activities” and do not have an explicit prohibition against soliciting for and getting paid for referrals, as long as the referrer plays no role in the mortgage loan process or negotiations besides the introduction, including any role in the application process.

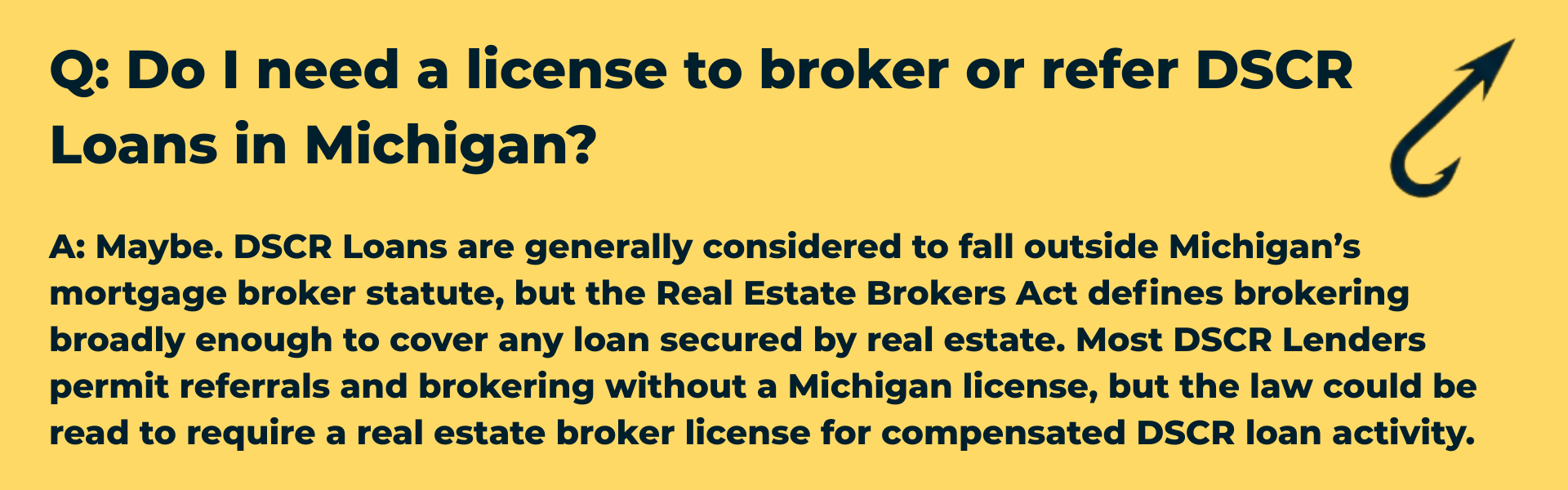

The state of Michigan has some complexity for DSCR brokers and referrers. The state’s Mortgage Brokers, Lenders, and Servicers Licensing Act (MBLSA, MCL § 445.1651 et seq.) regulates “residential mortgage loans” defined as “loans made primarily for personal, family, or household use.” By that consumer-purpose definition, DSCR loans are outside the MBLSA and do not trigger a Michigan mortgage broker license requirement. However, Michigan’s Real Estate Brokers Act (MCL § 339.2501 et seq.) defines a real estate broker to include anyone who, “for another and for a fee, commission, or other valuable consideration, negotiates a loan secured by real estate.” That broader definition sweeps in DSCR loans, since they are still loans secured by real property, even if business-purpose. In practice, most DSCR Lenders allow brokering in Michigan without enforcing the real estate broker license requirement, but the statutory language leaves room for regulators or conservative lenders to insist on compliance.

Q: Do I need a license to broker or refer DSCR Loans in Michigan?

A: Maybe. DSCR Loans are generally considered to fall outside Michigan’s mortgage broker statute, but the Real Estate Brokers Act defines brokering broadly enough to cover any loan secured by real estate. Most DSCR Lenders permit referrals and brokering without a Michigan license, but the law could be read to require a real estate broker license for compensated DSCR loan activity.

The state of Minnesota regulates consumer-purpose mortgage activity under the Residential Mortgage Originator and Servicer Licensing Act (Minn. Stat. Ch. 58), which defines a “residential mortgage loan” as “one made primarily for personal, family, or household use.” By that definition, DSCR Loans are outside the scope of Chapter 58 and do not trigger a mortgage originator license. However, Minnesota’s Real Estate Brokers Act (Minn. Stat. Ch. 82) defines a “real estate broker” to include anyone who, “for another and for a fee, commission, or other valuable consideration, arranges or attempts to arrange a loan secured by real estate.” That means DSCR loans, though business-purpose and not “consumer,” can still fall under the state’s real estate broker licensing rules. In practice, most DSCR Lenders allow referrals and brokering in Minnesota without enforcing the real estate broker license requirement, but the statute leaves enough ambiguity that conservative lenders may take a stricter stance.

Q: Do I need a license to broker or refer DSCR Loans in Minnesota?

A: Maybe. DSCR Loans are generally considered to fall outside Minnesota’s consumer mortgage law, but the Real Estate Brokers Act covers arranging any loan secured by real estate. Most DSCR Lenders permit brokering and referrals without a Minnesota license, though the statute could be read to require a real estate broker license for compensated DSCR loan activity.

The state of Nevada is famous for (well, at least in mortgage industry circles) having strict regulations on mortgage lending, including for DSCR Loans, and one of the few states that you will likely see carved out of a DSCR lender’s lending map when they are otherwise a national loan provider (along with the Dakotas). The applicable Nevada law (NRS 645B) has a different methodology of definitions than most other states, not specifically defining “mortgage broker” but rather having a broader definition of “mortgage company” which includes a person who, directly or indirectly “holds himself or herself out for hire to serve as an agent for any person in an attempt to obtain a loan or “who has money to lend” on “real property.” There are extensive requirements for a person to obtain a license listed out in “NRS 645B.410” and these rules are generally universally viewed as covering DSCR Loans.

In addition, Nevada even requires brokers (as well as direct lenders who don’t meet a strict “wholesale lender carve-out”) to have a physical in-state office and extensive licensing requirements and even fees, experience and net worth hurdles. It is safe to say that mortgage brokers, even when dealing with business-purpose residential mortgage loans like DSCR Loans, need to stay away from the Silver State when conducting broker business except if they are fully licensed and a Nevada resident. Even referrers should tread lightly and not gamble on loose interpretations as Nevada is one of the strictest regulators when it comes to mortgage loans, although simple referral handoffs to lenders may be okay if just incidental.

Q: Do I need a license to broker or refer DSCR Loans in Nevada?

A: Yes. Nevada’s mortgage laws (NRS 645B) have some of the strictest licensing requirements in the country and are generally interpreted to cover DSCR loans. To broker a DSCR Loan in Nevada, you must hold a state Mortgage Company license, maintain a physical in-state office, and meet significant experience, net worth, and fee requirements. Even referrals can be risky as Nevada regulators take a hard line on unlicensed activity, so compensation for introductions may be treated as brokering unless it is clearly incidental.

The state of New Jersey takes an unusual approach compared to most states. The New Jersey Residential Mortgage Lending Act (RMLA, N.J. Stat. Ann. § 17:11C-51 et seq.) defines a “residential mortgage loan” as “one made primarily for personal, family, or household purposes.” By that consumer-purpose definition, DSCR loans are outside the scope of the RMLA. However, New Jersey’s Real Estate Brokers Act requires a state real estate broker license to negotiate or arrange any loan secured by real property if not otherwise covered by the RMLA. In practice, this means that while a traditional mortgage broker license is not triggered for DSCR loans, arranging or referring these loans for compensation is generally viewed as real estate brokerage activity, requiring an NJ real estate broker license. While New Jersey law could be read to require a real estate broker license for DSCR brokering, in practice most DSCR Lenders treat DSCR loans as outside the mortgage licensing regime and allow brokers and referrers to operate without a state license.

Q: Do I need a license to broker or refer DSCR Loans in New Jersey?

A: Generally, no. DSCR loans fall outside New Jersey’s consumer mortgage act, and most wholesale lenders allow referrals and brokering without a state license. However, the Real Estate Brokers Act could be read to require a real estate broker license for arranging loans secured by real property, so a few conservative lenders may take the stricter view.

The state of North Dakota uses the North Dakota Money Brokers Act NDCC Chapter 13-04.1 to cover DSCR Loans, and defines “money brokering” as “the act of arranging or providing loans or leases as a form of financing, or advertising or soliciting either in print, by letter, in person, or otherwise, the right to find lenders or provide loans or leases for persons or businesses desirous of obtaining funds for any purposes” and requires specific licensing from the state commission, the North Dakota Department of Financial Institutions via the NMLS to originate or broker DSCR Loans in the state. While Chapter 13-10 of the North Dakota code appears to define “residential mortgage loans” as consumer-only, the overwhelming majority of DSCR Lenders interpret the state’s strict money brokering regulations to cover DSCR Loans, and indeed, in August 2025, new legislation in the North Dakota legislature continued to clarify in this direction. In sum, most national DSCR Lenders don’t even go through the cumbersome requirements to obtain licensing to originate DSCR Loans in North Dakota themselves, let alone allow independent mortgage brokers or referral partners to earn compensation through referring loans to them there. As such, North Dakota appears to be a state where referring DSCR Loans, unless fully licensed in the state, is not allowed.

Q: Do I need a license to broker or refer DSCR Loans in North Dakota?

A: Yes. North Dakota regulates DSCR loans under the state’s Money Brokers Act (NDCC Chapter 13-04.1), which requires a license from the Department of Financial Institutions through NMLS to arrange, negotiate, or even solicit loans for compensation. While the state’s Residential Mortgage Act applies only to consumer loans, DSCR loans fall under the broader “money brokering” definition. As a result, most lenders exclude North Dakota from DSCR programs, and unlicensed referral fees are not permitted.

The state of Oregon has similar rules and regulations to its eastern neighbor in Idaho, with applicable definitions and requirements found in the “Oregon Mortgage Lender Law” or ORS 86A.095 to 86A.198. Oregon has a somewhat broad definition of “mortgage broker” but it includes someone who “for compensation, or in the expectation of compensation, either directly or indirectly makes, negotiates or offers to make or negotiate a mortgage loan” with the applicable definition of “residential mortgage transaction” to cover DSCR Loans, which covers mortgages for a “property upon which four or fewer residential dwelling units are…situated.” And the code states plainly that it “is unlawful for any person to engage in residential mortgage transactions in this state as a mortgage banker or mortgage broker unless the person is licensed.” As such, it is pretty clear that an Oregon NMLS license is required to act as a broker for mortgage loans in Oregon, including DSCR Loans, but simple “referrals” in which no “negotiations” occur, rather only include a simple handoff or introduction, could reasonably be interpreted by many parties as okay under the state statutes, since there is no “solicitation” language found in these regulations.

Q: Do I need a license to broker or refer DSCR Loans in Oregon?

A: Yes. Oregon law requires a Mortgage Lender/Broker license (through NMLS and the Department of Consumer and Business Services) to receive compensation for “residential mortgage transactions,” which include DSCR Loans on properties with four or fewer residential units. The statutes define brokering broadly, making, negotiating, or offering to negotiate a mortgage loan, so an Oregon license is required for brokering DSCR loans. However, because there is no explicit prohibition on referrals or solicitation language in the law, some interpret that a pure introduction without involvement in the loan process or negotiations may fall outside the licensing requirement.

The state of South Dakota is typically treated the same by DSCR Lenders as its northern neighbor and Dakota namesake, commonly excluded from otherwise national DSCR lending programs, due to the combination of its sparse market and strict lending regulations. South Dakota defines “residential mortgage loans’ to specifically only apply to mortgage loans for consumer use (i.e. owner-occupancy, not rental or business-purpose) while Section 54-14-13.5 offers a specific license requirement for “nonresidential mortgage loans,” which while not explicitly defined, can reasonably be assumed to include DSCR Loans. Interestingly, the brief statute states that “any individual acting as an intermediary, on behalf of a company licensed as provided in this section, shall be disclosed to the director during the application process and annually thereafter” meaning that someone who brokers, or potentially even refers DSCR Loans in South Dakota to a licensed lender, must be disclosed initially and annually by the lender in the state. As such, while the regulations may be relatively amenable for unlicensed brokers and referrers in the Mount Rushmore State, the combination of low volume of eligible rental properties and potentially cumbersome annual reporting requirements make it an uncommon state for brokers or referrers of DSCR Loans to focus on.

Q: Do I need a license to broker or refer DSCR Loans in South Dakota?

A: Yes. South Dakota requires a license under SDCL 54-14-13.5 for “nonresidential mortgage loans,” which are generally interpreted to include DSCR loans. The law also requires disclosure of anyone acting as an intermediary, so even referrals must be tied to a licensed lender.

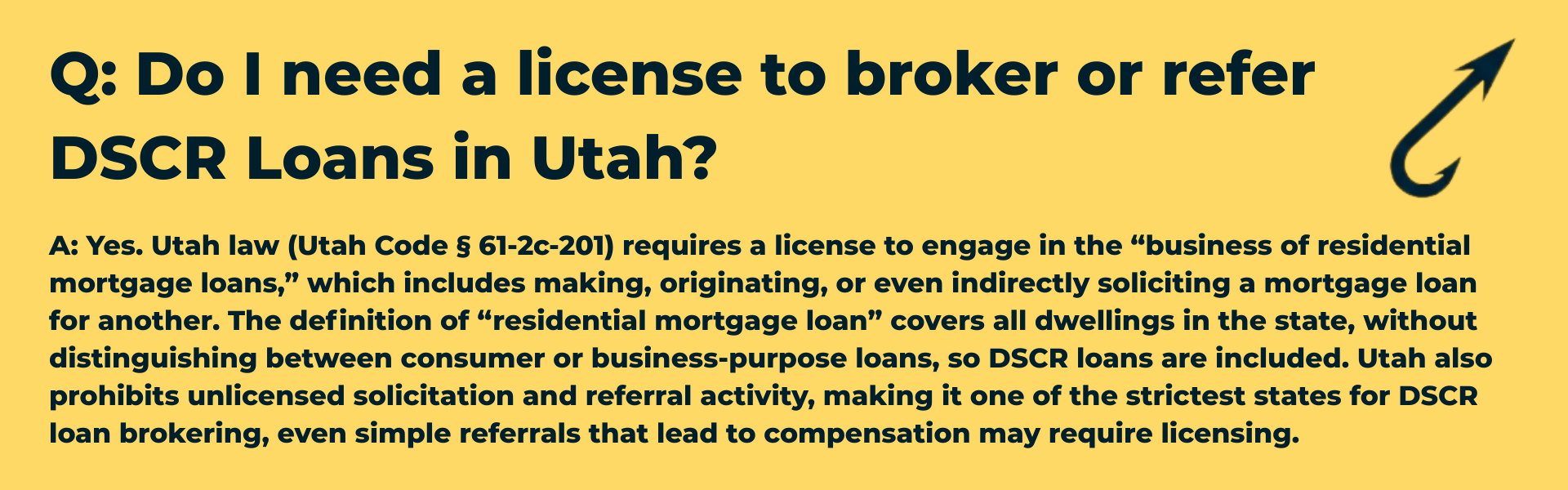

In the state of Utah, the regulations cover what they define as the “business of residential mortgage loans” which includes compensation for making or originating a residential mortgage loan and includes “directly or indirectly solicit a residential mortgage loan for another.” To do so, individuals must “obtain a license” per 61-2c-201(1). And to tie it together, the definition of “residential mortgage loan” does not differentiate between mortgage loans for occupancy or consumer use versus business purpose use, rather broadly covers “dwellings located in the state.” As such, Utah has some of the strictest regulations over DSCR Loans brokering and referring in the country, and any entity or person seeking to broker DSCR Loans in Utah should be fully NMLS-licensed. Additionally, with prohibitions on “soliciting for another,” anyone considering even simply referring DSCR Loans should tread lightly and consult an attorney before any sort of promotional activities leading to compensation for referring loans to lenders in the Beehive State.

Q: Do I need a license to broker or refer DSCR Loans in Utah?

A: Yes. Utah law (Utah Code § 61-2c-201) requires a license to engage in the “business of residential mortgage loans,” which includes making, originating, or even indirectly soliciting a mortgage loan for another. The definition of “residential mortgage loan” covers all dwellings in the state, without distinguishing between consumer or business-purpose loans, so DSCR loans are included. Utah also prohibits unlicensed solicitation and referral activity, making it one of the strictest states for DSCR loan brokering, even simple referrals that lead to compensation may require licensing.

The state of Virginia is one of the few “gray area” jurisdictions when it comes to DSCR loan referrals and licensing. The Virginia Mortgage Lender and Broker Act (Va. Code § 6.2-1600 et seq.) defines a “mortgage loan” as a loan to an individual primarily for personal, family, or household use secured by a 1–4 unit dwelling. By this definition, business-purpose DSCR loans are technically outside the Act. As such, many DSCR Lenders allow brokers and referrers to operate in Virginia without a Virginia mortgage broker license. However, because the statute also references “residential real property” in several places, some conservative lenders take the position that a license is required if compensation is tied to arranging loans secured by 1–4 unit dwellings, regardless of purpose. In practice, the majority view in the market is that DSCR Loans do not require a Virginia mortgage broker license, but brokers and referrers should be aware that compliance interpretations can vary and may change as regulators provide further guidance.

Q: Do I need a license to broker or refer DSCR Loans in Virginia?

A: Probably not. Virginia’s Mortgage Broker Act applies only to consumer-purpose loans, so DSCR loans are generally treated as exempt. Most lenders allow referrals and brokering without a Virginia license. That said, because the statute references loans secured by residential property, some lenders take a stricter view, so brokers should confirm compliance policies before marketing DSCR loans in the state.

In summary, for brokering or referring DSCR Loans for compensation, there are 38 states in which it appears smooth sailing for anyone to enter the world of referring or brokering business-purpose loans without NMLS licensing common for consumer or standard mortgage lending. The states of Arizona, Idaho, Nevada, Oregon, Utah, North Dakota and South Dakota appear to be no-go zones for unlicensed brokers, even for business-purpose DSCR Loans, although in these states, plus California, it may be okay for simple handoff referrals where compensation is received strictly for making an introduction and playing no role in the actual loan application or negotiation process. Finally, the states of New Jersey, Michigan, Minnesota and Virginia have rules outside of mortgage brokering regulations but related to real estate brokering that may come into play regarding brokering or referring DSCR Loans but remain gray areas and differ from lender to lender.

Note: This discussion is provided for general informational and educational purposes only and does not constitute legal advice. State mortgage and real estate licensing laws are complex, subject to change, and open to interpretation. You should not rely on this summary to make business, compliance, or licensing decisions. Before brokering, referring, or receiving compensation for DSCR loan activity in any state, consult with qualified legal counsel and verify requirements with the appropriate state regulator.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.