.png)

By now, it’s clear why DSCR loans became the rocket fuel of the STR industry. But even rocket fuel comes with handling instructions. Short term rentals bring their own set of quirks that trip up unsuspecting investors; these are the kind of details that can derail a DSCR deal if not planned for in advance. This section will cover things that every investor should keep on their radar when approaching DSCR Loans for short-term rentals.

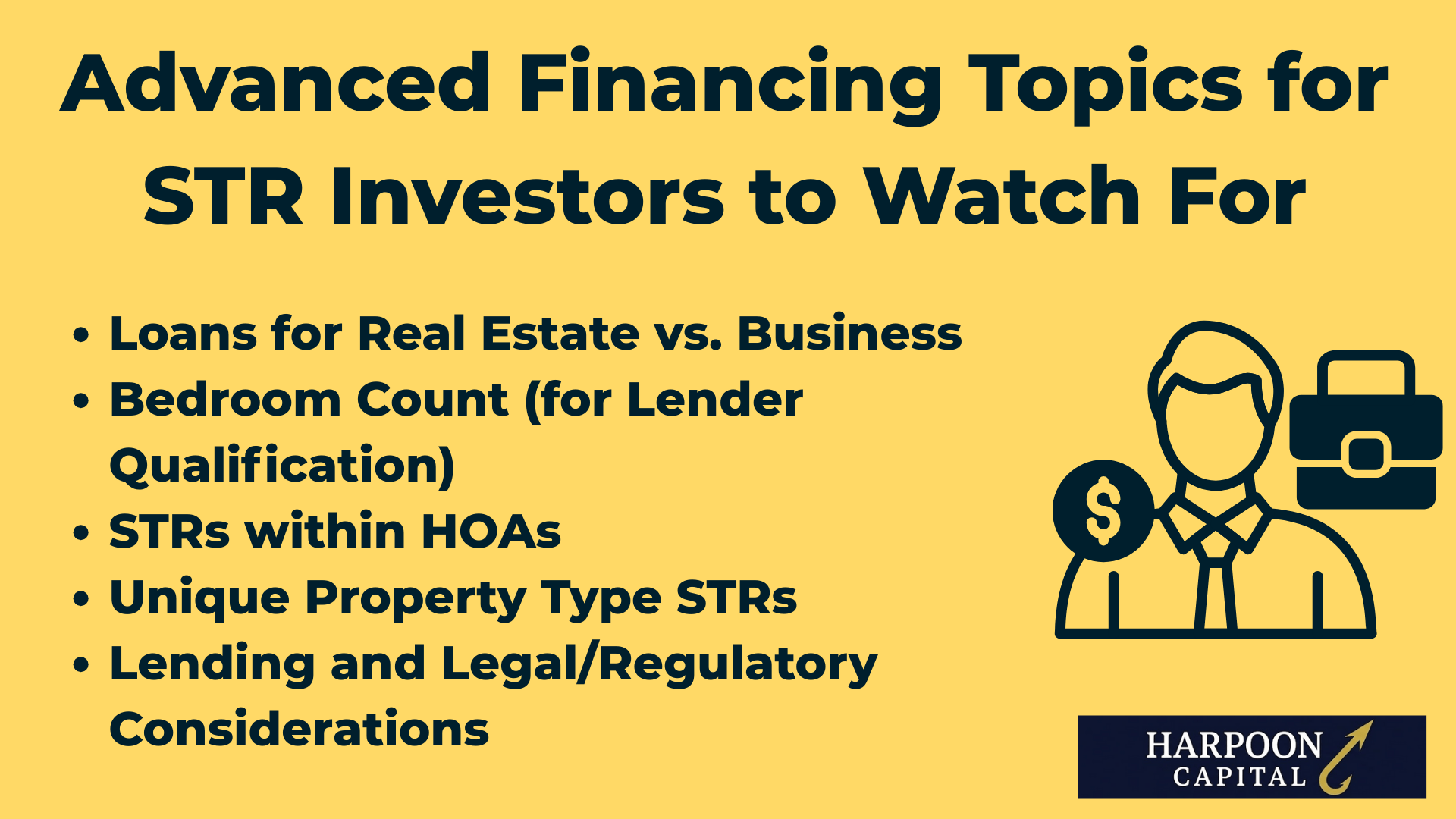

We'll cover five key issues for advanced STR investors to be aware of, things that can be the difference between a successfully financed STR and being stuck in STR financing limbo.

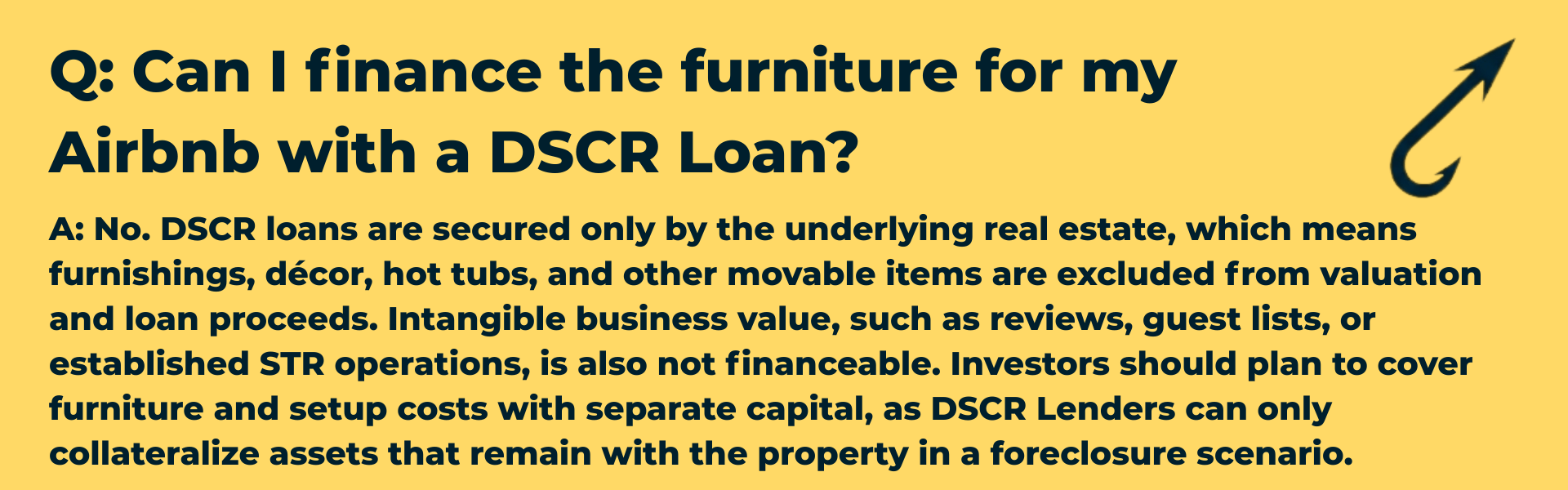

One common problem that real estate investors investing in short term rentals frequently encounter is the value discrepancy between a thriving short term rental and the property that is the setting for the thriving short-term rental. Successful STRs aren’t just a great property – performance and profitability come from many other aspects as well – the furnishings and amenities, the hard-earned five-star reviews and Airbnb “Superhost” status and the loyal guests who book again and again after tremendous experiences. Nobody who is serious about STRs disputes this reality.

However, this reality (STRs are more than just a property) runs into another reality; DSCR Loans are mortgage loans and secured by residential real estate. Meaning, DSCR Loans, by far the best financing option available for STR investors, strictly finance real property, and not “chattel” like furniture and movable amenities or intangibles like review histories and guest-lists. This is because at the end of the day, DSCR Lenders are underwriting loans with the ability to foreclose (and take over the property) if things go wrong (i.e. borrower default) as their key risk mitigant, and this is a huge factor in what allows them to offer such borrower-friendly financing terms. In case of foreclosure, DSCR Lenders can’t be sure to be able to “foreclose on” or take ownership of non-real estate items (owners can easily take couches, TVs, even hot tubs or big-ticket items) with them, not to mention their Airbnb host profiles and guest lists. As such, DSCR Lenders cannot “give credit to” or lend on anything besides the real, built into the ground real estate.

Among the many creative and innovative strategies that have sprung up among STR investors as the industry grows and matures is the development and sales of “turnkey” STRs. This describes the practice of investors buying up-and-running short term rentals that already have the property performing professionally, i.e. fully furnished with great amenities, attention-grabbing professional pictures, listings optimized with top reviews and ratings, etc. For buyers chasing passive income, buying these truly turnkey STRs is very appealing, an opportunity to earn money with a true “hands off” approach. While this is a relatively new phenomenon for STRs, this practice is a long-time fixture of commercial real estate, where “real estate developers” is an entire class of professionals whose specialty is building or renovating and getting properties up and running to “stabilization,” and then selling to another class of investor who excels at managing stabilized properties, each an expert and focus on their top competence.

The problem that occurs, however, is that unlike commercial lenders, DSCR Lenders can’t lend on anything besides the true residential real estate. Valuation also must be derived from the sales comparison approach versus the income-based approach, which CRE lenders can typically rely on. This creates situations where passive-income driven buyers are willing to pay a fair price for a full-service STR business – a deal that makes sense for buyer and seller – but can only get financing (via DSCR Loan) on the value of the real estate.

For example; a property may be a fully turnkey short-term rental developed by expert operators using the latest hot amenities like a pickleball court or hot tub, and have the recent revenue numbers and bookings to prove the success of the venture. While the real estate is worth $1,000,000 – it’s being sold as-is with all the furnishings, reviews, photos and even management transferred over, and that is worth – both to buyer and seller – another $250,000 – for a total agreed-upon price of $1,250,000. The problem, however, is that the DSCR Lender can only lend on the value of the property – in this example, $1,000,000 – since in case something goes wrong (i.e. default), they can only be assured of taking over a property worth $1,000,000 on the open market (to all potential buyers, STR investors and owner-occupants alike) with no ability to attain all the other bells and whistles being sold. So the DSCR Lender can only, assuming a 75.0% maximum LTV for STR Loans, lend $750,000 for the purchase, meaning the buyer needs to come up with not only the $250,000 down payment but also the additional $250,000 for the total price that includes the valuable (to them) additional items like furnishings, etc.

Unfortunately, there really isn’t a solution on the horizon for these situations, which are sure to increase as the STR industry enters the “later innings” of maturity, and begins to more and more resemble more traditional commercial real estate investment strategies and specializations. DSCR Loans will continue to be ideal for financing the real estate portion of these transactions (it’s not an issue for DSCR Lenders if the borrower is paying additional amounts for furnishings or intangibles), however passive income STR investors will need more capital or alternative (unsecured) financing sources to buy these types of properties. It’s likely too that as the industry matures, more business-based or commercial financing options will emerge to cover this portion of the market while DSCR Lenders will not be the sole option for these turnkey sales, but for now represents an underserved portion of the STR financing landscape.

Q: Can I finance the furniture for my Airbnb with a DSCR Loan?

A: No. DSCR Loans are secured only by the underlying real estate, which means furnishings, décor, hot tubs, and other movable items are excluded from valuation and loan proceeds. Intangible business value, such as reviews, guest lists, or established STR operations, is also not financeable. Investors should plan to cover furniture and setup costs with separate capital, as DSCR Lenders can only collateralize assets that remain with the property in a foreclosure scenario.

In the world of short-term rentals, how many people a property can “sleep” is often as important as its location and features. On Airbnb, a four-bedroom home marketed with bunk beds, sofa sleepers, and a finished loft might brand itself as a “sleeps 14” retreat, and platforms like AirDNA will translate that guest capacity directly into revenue projections. Because most DSCR lenders now rely heavily on AirDNA Rentalizer reports for qualification, bedroom and guest count have become a critical driver in whether a deal pencils out. A rule of thumb has emerged in DSCR Loan underwriting: two guests per legal bedroom.

The catch is that what qualifies as a “bedroom” in the eyes of appraisers and local building codes is much narrower than what hosts market online. Appraisers generally require a closet, proper egress windows, and that the room be above ground (no basements or converted garages without permits). For long-term renters or owner-occupants, these rules make sense: a bedroom needs closet space and safety features for daily use. But STR guests arriving with only a suitcase don’t typically care whether a closet exists, they care whether there’s a bed. This creates a recurring mismatch: what functions as a “bedroom” for Airbnb guests may not be recognized as one for an appraiser, and consequently for DSCR Lender qualification.

Some DSCR Lenders, aware of this gap, have developed case-by-case workarounds. If an appraisal includes photos clearly showing a non-traditional space being used as a bedroom (for example, a loft staged with beds), certain lenders may allow it to be counted toward guest capacity in AirDNA-based underwriting. In some cases, lenders may even accept evidence from completed bookings, such as an Airbnb record showing twelve guests stayed in a three-bedroom home, with a positive review, to justify a higher guest count than the appraisal alone would suggest. But DSCR Lender rules and judgments in this area can diverge and be fluid, so it’s important to clarify this as quickly as possible if it may apply.

Q: How many guests can I qualify for on a DSCR Loan for an Airbnb?

A: DSCR Lenders that use AirDNA projections typically apply a two-guests-per-legal-bedroom rule when calculating income. That means an Airbnb marketed as “sleeps 14” will only qualify based on the appraiser’s legal bedroom count, not extra bunks, lofts, or makeshift sleeping spaces. Because guest count drives projected revenue, this rule can significantly affect how much financing a property qualifies for.

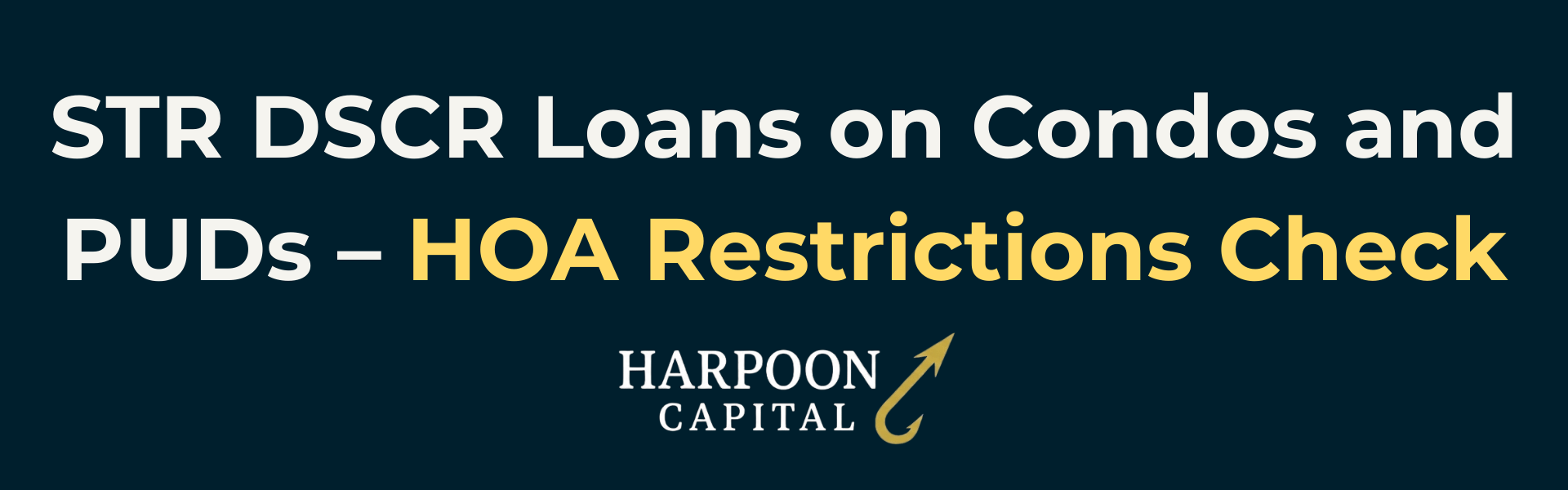

Short-term rentals in condominiums and planned unit developments (PUDs) are generally financeable with DSCR loans, but they carry an additional layer of risk: the rules of the homeowners’ association (HOA). Most condo and PUD projects already impose some degree of rental restrictions, for example, capping the number of units that can be used as investments, requiring owners to obtain rental permits or limiting overall investor concentration. These limits are standard considerations in underwriting and surface during the condo questionnaire or appraisal review.

For STR investors, however, there is an extra hoop: many associations adopt short-term rental–specific restrictions on top of the usual rental usage limits. These may take the form of outright bans on nightly rentals, minimum lease-length requirements (30 days, 90 days, or more), or special permits that must be secured before operating on platforms like Airbnb or VRBO. If such restrictions exist, they will be flagged during underwriting, and a property marketed as an STR that cannot legally operate as one will not qualify for DSCR Loan, and wouldn’t be a smart investment either!

Q: Will my HOA stop me from using a DSCR Loan for a short-term rental?

A: Possibly. Most DSCR Lenders require confirmation that short-term rentals are permitted by the homeowners’ association, and many HOAs impose restrictions such as minimum lease lengths, rental caps, or outright bans on nightly rentals. If STR use is prohibited, the property will not qualify for STR financing, regardless of whether other owners are listing. Always review HOA bylaws up front to avoid wasting time and money on a deal that cannot be underwritten.

One of the defining features of the STR market is its creativity. Log cabins in the Smokies, A-frames in Tahoe, yurts, tiny homes and treehouses can often outperform traditional housing stock on platforms like Airbnb and VRBO, commanding premium nightly rates through novelty, Instagram appeal, and experiential travel trends. But DSCR Lenders, unlike guests, value predictability.

From an underwriting perspective, “unique” often translates into “ineligible.” DSCR Loans generally must be secured by residential real estate that can function as a full-time dwelling. That means properties must meet habitability standards and be comparable to other year-round residences. Yurts, treehouses, tiny homes, and similar “glamping” structures fail this test. They may crush it online, but they do not qualify as collateral in the eyes of pretty much all DSCR Lenders. Even appraisers, required to find “like-kind” sales, struggle to assign defensible value to these assets.

Q: Can I get a DSCR Loan for a treehouse, yurt, or other unique Airbnb property?

A: No. DSCR loans universally exclude glamping units, yurts, treehouses, and similar non-standard properties because they cannot be considered full-time residential real estate. While these properties may generate exceptional STR returns, they fall outside DSCR loan eligibility and must be financed with cash or alternative lending.

If there’s one wild card every STR investor must contend with, it’s local regulation. Unlike multifamily or office properties, short-term rentals live in a shifting legal gray zone where rules can vary block by block and change from year to year. For much of the 2010s, STRs thrived in a vacuum of regulatory oversight, cities didn’t know how to classify them, zoning codes didn’t anticipate them, and enforcement was light. But those “wild west” days are over.

Over the last several years, municipalities across the U.S. have moved toward a middle ground between free-for-all markets and outright bans. Few cities want to eliminate STRs entirely, but most also want to manage them. The result is a patchwork of rules: permit requirements, inspections, local lodging taxes, and sometimes caps on the number of units in a given area. Austin, Texas is a good example of this trajectory. Initially, the city imposed broad restrictions and aggressive enforcement, and only after a Federal Court struck down the draconian rules, evolved towards a permit-based system where STRs are legal, taxable, and heavily tracked. Investors there can still operate successfully, but only if they play within the system. This is the likely future in most markets: some bureaucracy, some costs, but workable rules that allow STRs to remain a permanent fixture.

For DSCR Lenders, these shifting laws present real underwriting challenges. In markets where STR use is clearly prohibited, New York City is the textbook case with Local Law 18, or certain zones in Nashville where new permits are frozen, DSCR Lenders will not qualify properties as STRs. They may qualify only on LTR market rental income, reduce maximum leverage, or simply decline the loan. But outside of obvious red-flag markets, most DSCR Lenders do not dive deeply into local regulations. Instead, they rely on borrower expertise, appraisals, HOA questionnaires, and even tools like AirDNA’s regulation scores to avoid banned areas. This is especially true for DSCR Lenders who cater to experienced “pro” STR operators, they expect that a borrower with a proven portfolio isn’t going to mistakenly invest in a market where STRs aren’t allowed.

While by 2026, it's fairly easy to find a DSCR Lender that will qualify a short term rental as a short term rental, i.e. utilize STR-based rental projections versus requiring the DSCR ratio to reflect long-term market rents, it’s not a bad idea for investors to evaluate this “Plan B,” or what the investment would look like if forced to rent it out for a traditional long-term (i.e. 12-month) leases. This “plan B” analysis can be valuable in any investment game plan (even if not used or required to qualify for a DSCR Loan), as while many jurisdictions are moving away from outright bans, none of these rules are really “set in stone” and could always change in the future, and some markets may indeed follow this anti-STR path. When comparing multiple options, picking a property with better projections in a potentially needed “Plan B” long-term rental scenario can be a smart consideration or tiebreaker.

Q: Can I get a DSCR Loan for an Airbnb in a city with short-term rental (STR) restrictions or permit rules?

A: Often yes, if STR use is permitted or permissible under local code; if it’s banned, lenders won’t qualify the property as an STR. DSCR Lenders don’t do deep legal reviews but will flag red-alert markets (e.g., NYC’s Local Law 18 or permit freezes in parts of Nashville), may haircut income or lower LTV, and rely on the appraisal, HOA/condo questionnaire, borrower attestations, and tools like AirDNA’s regulation score. Confirm the permit path up front, DSCR Lenders underwrite the collateral, not your compliance, and a missing or ineligible permit can sink the loan late in the process.

Up Next: Using DSCR Loans for the BRRRR Strategy!

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.