.png)

When buying an investment property, you’re not just purchasing the land and residence (the “improvements”), you’re also taking on the property’s legal history. Title work is the process DSCR Lenders use to verify that the property securing your DSCR loan has clear, insurable ownership and that their lien will be in first position, free from competing claims.

The way that verification is formalized is through title insurance. Title insurance protects against losses from defects in the property’s title that were unknown at closing, such as undiscovered liens, recording errors, fraudulent deeds, or unresolved ownership claims. Unlike other types of insurance that protect against future events, title insurance protects against past events that could threaten your ownership or the lender’s lien. Title insurance is both the borrower’s safety net and the DSCR Lender’s safety net against surprise ownership or lien problems from the past.

Title insurance protects both the borrower and the lender from problems with the property’s ownership history that could cost time, money or even the property itself.

Without it, serious issues could occur, including an old lien resurfacing, such as a past lender, contractor, or tax authority claiming they are still owed money from even before you owned the property. There could also be ownership disputes, where a missing signature, forged deed, or unrecorded transfer could let someone else claim they have rights to the property or create messy inheritance claims after the death of a family member. Additionally, there could be boundary or easement problems, such as a neighbor claiming part of the land you think you own, or a utility could demand access that affects your use of the property.

Q: Why do DSCR Lenders require title insurance?

A: Title insurance protects both the lender’s lien position and your ownership rights against hidden title defects, recording errors, or undiscovered claims that could surface after closing. In DSCR lending, where investment properties often have complex ownership histories or multiple past transfers, the risk of something being missed in public records is higher, and title insurance is the safeguard that ensures your property and financing are secure.

Once your DSCR loan moves into processing, the DSCR Lender will typically order the title work. This starts the process of researching the property’s ownership history, checking for liens, and preparing the title commitment. In many states, the buyer or borrower has the legal right to choose the title company. In practice, however, the selection is often influenced by local custom as some markets have “go-to” title companies that handle the majority of transactions. Additionally, it could be determined in the purchase contract, i.e. sometimes the seller specifies the title company in the agreement. The choice could also come down to lender requirements as well, as many DSCR Lenders have an approved list of title providers based on past experience or trust, and may not do a DSCR Loan with unapproved title companies (typically companies that they had problems with in the past).

Even if you have a preferred title provider, your DSCR Lender may require that the company be on their approved vendor list. This ensures the title insurer meets the lender’s standards for financial stability, policy coverage and secondary market acceptance (i.e. also okay with their loan buyers and the eventual note holders). In some cases, if a chosen company is not approved, the DSCR Lender can request they go through an approval process, but this can add time and uncertainty to your closing timeline, and is usually not worth the hassle, since there is not too much difference among title companies, as it’s a tightly regulated, mostly commoditized industry.

For DSCR Loans, and really all mortgage loans, the title process usually begins right after the term sheet is signed, around the same time the DSCR Lender orders the appraisal, a step often referred to as “opening title.” The DSCR Lender places the order with a title company to start researching the property’s ownership history and any recorded claims.

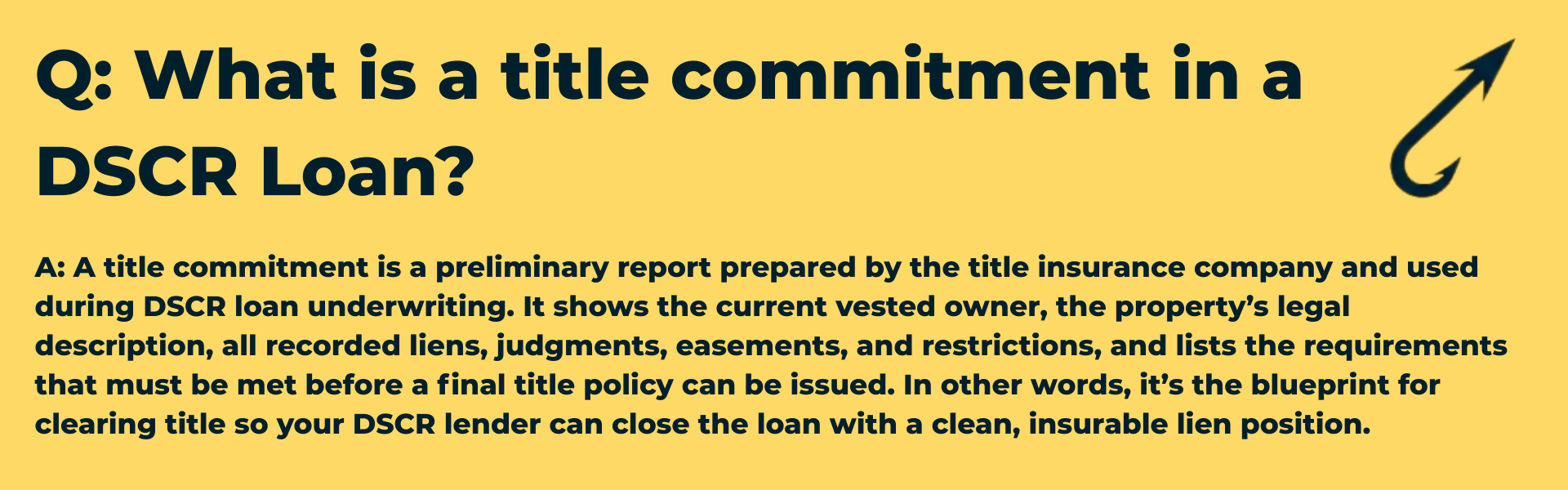

The first deliverable from that process is the Title Commitment. This is the document the lender uses during underwriting to confirm who currently owns the property (vested owner), the legal description of the property in official records, all recorded liens, mortgages, judgments, easements and any restrictions, covenants, or encroachments that could affect use. It will also include a checklist of requirements that must be satisfied before the title company will issue final title insurance.

While the appraisal fee is almost always charged to the borrower upfront, the cost for title work is almost always paid at closing. In most cases, the exact amount isn’t finalized until near the end of the process when the settlement statement is prepared.

Once the loan has closed and funded and the security instrument (mortgage or Deed of Trust) is recorded, the title company issues the Final Title Policy. This is the binding insurance contract that confirms the DSCR Lender’s lien is in first position, protects the lender (and the borrower, if an Owner’s Policy is purchased) against covered title defects and serves as permanent evidence that all the requirements from the Title Commitment have been satisfied. If, for any reason, a DSCR Loan does not close after title has been opened, the lender will almost always absorb (“eat”) the title costs, and the borrower will not be billed.

In summary, the Title Commitment is the preliminary report used for underwriting, showing what needs to be cleared before closing and the Final Title Policy is the actual insurance contract issued after closing that locks in lien priority and coverage, issued usually a couple weeks after the loan closes and funds, and changes hands if the transaction is a purchase.

Q: What is a title commitment in a DSCR Loan?A: A title commitment is a preliminary report prepared by the title insurance company and used during DSCR loan underwriting. It shows the current vested owner, the property’s legal description, all recorded liens, judgments, easements, and restrictions, and lists the requirements that must be met before a final title policy can be issued. In other words, it’s the blueprint for clearing title so your DSCR lender can close the loan with a clean, insurable lien position.

For DSCR Loans, who is responsible for clearing title issues depends on whether the transaction is an acquisition or a refinance. For acquisitions, clearing title issues are the seller’s responsibility, who must deliver the property with clear, insurable title. If problems are found, the seller (through their title company or attorney) must resolve them before the sale can close. The buyer’s role (i.e. borrower on a DSCR Loan that’s an acquisition) is to monitor the process, push for resolution and decide whether to proceed if issues aren’t fixed in time.

For refinances, since the borrower already owns the property, the borrower is responsible for curing any title issues before the DSCR Lender can close. This can mean paying off liens, updating entity documentation or providing proof of prior mortgage satisfactions yourself.

Q: Can title issues delay closing on a DSCR Loan?

A: Yes, title issues are one of the most common causes of closing delays. Problems like unreleased prior mortgages, unpaid property taxes, judgments, or missing ownership documents must be resolved before the final title policy can be issued. In DSCR loans, delays can also occur if entity documentation doesn’t match the name in the title commitment, so reviewing and addressing issues early is critical.

The Title Commitment format can vary slightly by state or title company, most commitments are organized into three main schedules plus some general terms.

Schedule A is the foundation of the title commitment. It answers the “who,” “what,” and “how much” of your transaction, and it’s the first place to check for obvious errors.

Key Elements of Schedule A of a Title Commitment for a DSCR Loan:

Schedule B-I lists the conditions that must be met before the title company will issue the final title policy. Think of it as the official “closing checklist” from the title insurer’s perspective.

Common requirements that may appear on Schedule B-I of a Title Commitment for a DSCR Loan can include:

Schedule B-II lists exceptions to coverage, things the title insurance policy will not protect against. These remain “attached” to the property after you buy or refinance it. It’s important to note that not all exceptions are a deal-breaker, many are normal and expected. But some can directly affect your investment strategy. For example, a private easement allowing a neighbor access through your parking lot could impact your ability to redevelop or reconfigure the property. Always ask your title officer to walk you through any exceptions you don’t fully understand.

Common exceptions featured on Schedule B-II of a Title Commitment for a DSCR Loan include:

Q: Should I buy an Owner’s Policy on an investment property when using a DSCR Loan?

A: While it’s optional, most real estate investors choose to purchase an Owner’s Title Policy when closing a DSCR Loan. It protects your ownership interest for as long as you hold the property, even after the loan is paid off, against covered title defects that could affect your ability to sell, refinance, or fully control the property. In investment properties, where future value and liquidity matter, that added protection can be well worth the one-time premium.

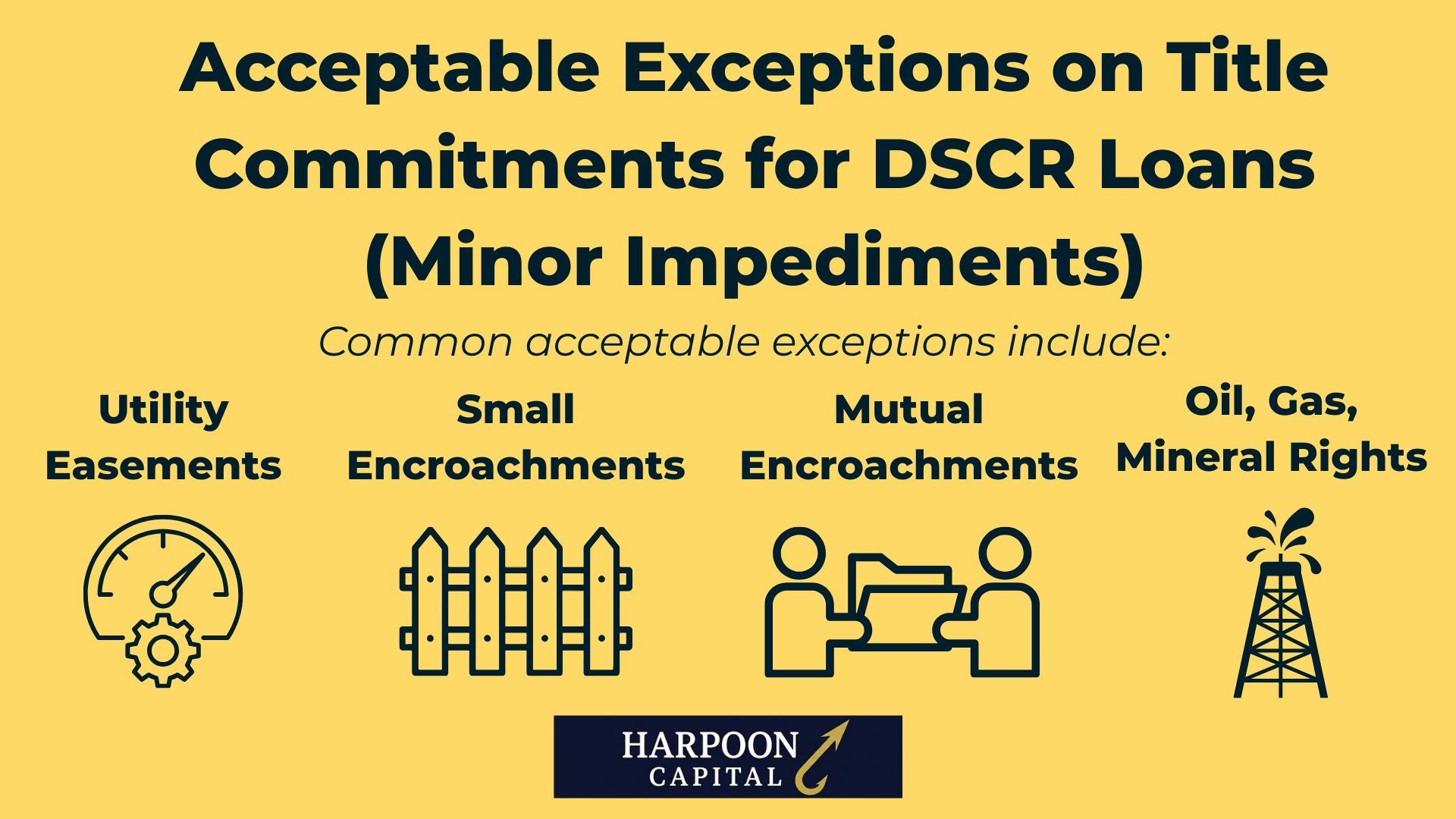

Not every exception listed in a Title Commitment is actually a problem for a DSCR Loan, some are considered normal and acceptable for closing. These “minor impediments” don’t impact your ability to use or improve the property, and they won’t stop a DSCR Lender from approving the loan. If an exception falls into these categories, it’s usually nothing to worry about, but always confirm with the title officer or lender representative if unsure.

Common acceptable exceptions include:

Some title exceptions can’t remain on record at closing unless they are affirmatively insured over with an ALTA endorsement, and in many cases, they must be removed entirely before a DSCR Loan can close.

Examples of unacceptable exceptions found on Title Commitments for DSCR Loans include:

.png)

A Private Transfer Fee Covenant is an agreement recorded against a property that requires a fee (often a % of the sales price) to be paid to a private third party every time the property changes hands, sometimes for decades.

Generally, covenants created on or after February 8, 2011, can create a lien that takes priority over the lender’s mortgage, which makes them unacceptable to most DSCR Lenders, and automatically ineligible for a DSCR Loan. This is because this was a date determined by the publication of the FHFA’s rule on PTFCs that utilized this date, effectively banning mortgage loans secured by properties with such covenants from being included in conventional mortgage loan securitizations. While DSCR Loans are from private lenders and not connected to agency MBS, most DSCR Lenders followed this industry standard and generally comprehensively avoid lending on properties with PTFCs, in line with conventional lender policy. If you see any language in your title documents about paying a private fee to a developer, HOA, or other third party upon sale – flag it immediately. It could make the property ineligible unless the covenant is removed.

.png)

Sometimes a title search shows a mortgage lien that should have been removed years ago, for example, after you or a prior owner paid off the loan. If the lien is still showing, it’s called an unreleased prior mortgage lien.

For DSCR Loans, prior mortgage liens must be removed from title before the DSCR Lender will close, unless the title company can verify in writing that it has been satisfied (zero balance confirmed) and is willing to insure over it. Note that this can include HELOCs and even if the HELOC balance is zero, a home equity line of credit must be formally closed and the lien released to prevent future draws for a DSCR Loan to be extended on the property.

For investors utilizing HELOCs, a common strategy, especially in high-rate environments where cash-out refinances aren’t viable, it’s smart to proactively formally close any HELOCs that may be long paid down to zero, but still technically open.

While many title issues can be resolved with a payoff, a recorded release, or an endorsement, some problems are so severe, costly, or time-consuming that they can completely derail a DSCR Loan. These “deal-killers” usually prevent the title company from issuing a final policy, which means the DSCR Lender cannot close. Below are some of the most common examples, why they matter and how they might appear in a title commitment.

Not every title issue kills a deal, but the ones above are either impossible to fix within the loan’s timeline or require costs and legal actions that outweigh the property’s value or projected return. Reviewing the Title Commitment early is the best way to spot these red flags before you invest time and money into a deal that can’t close.

The earlier you review your title commitment, the better your chances of spotting these red flags before you’ve invested significant time or money into a DSCR Loan application. If you see anything in the commitment that looks unusual, out of place, or costly to fix, raise it with your DSCR Lender and title company immediately. In some cases, walking away early is the smartest financial move, and the only way to do that confidently is by understanding what you’re reading.

In addition to the standard title insurance policy, many DSCR Lenders require ALTA (American Land Title Association) endorsements, add-ons that provide extra coverage for specific property types or risks. These endorsements modify the base policy to address issues unique to the property’s legal structure or intended use.

Common endorsements in DSCR Loans include ones for condo units and properties within PUDs (planned unit developments). The ALTA 4 / 4.1 – Condominium Endorsements which ensures the condo unit’s title is valid and insurable under the condo declaration. It also confirms the DSCR Lender’s lien covers the unit and its undivided interest in common areas. ALTA 4.1 adds coverage for future violations of covenants or restrictions not caused by the insured. ALTA 5 / 5.1 – Planned Unit Development (PUD) Endorsements, covers risks specific to PUDs, such as ownership rights in common areas and the enforceability of covenants. ALTA 5.1 expands coverage to include violations of restrictive covenants not caused by the insured.

Other common endorsements found on title for DSCR Loans include ALTA 8.1 – Environmental Lien Endorsement, which protects against loss if a recorded environmental lien (e.g., for contamination cleanup costs) is not listed in the title commitment but later affects the property. ALTA 9 – Restrictions, Encroachments, Minerals offers coverage for losses due to certain violations of covenants, encroachments onto the property or mineral rights issues.

A Tax Certificate is an official document from the county or municipal tax office confirming the property’s current year tax amount, whether taxes are paid or unpaid, any delinquencies or penalties and critical details on due dates and installment schedules. This information is important for DSCR Loans since property tax amounts are a key number in the DSCR calculation (the “P” in “PITIA”). Additionally, most DSCR Loans utilize an escrow for property taxes, and the tax certificate provides the exact figures to establish the monthly reserve and upfront deposit.

Whether property taxes appear in the Title Commitment depends mostly on state and county systems, with some additional variation in title company practices. In many states and larger counties, property tax data is integrated into the public records database the title company searches, so the tax amount shows up automatically. In other areas, especially where tax collection is handled by separate municipalities or special districts, the title company’s standard search may not include tax details, so they must order them separately. Even in states where taxes are usually included, if the search is done early and the new year’s bill hasn’t been issued yet, the title commitment may list the tax amount as “TBD,” prompting a separate Tax Certificate order later.

Generally, for about half to two-thirds of DSCR Loans, the Title Commitment will show the tax amount. In the rest, the lender or title company will order a Tax Certificate during underwriting. If ordered, it comes directly from the taxing authority (or their contracted vendor) and is considered a “sometimes needed” document.

A Warranty Deed is the legal document that transfers ownership of a property from one party (the grantor) to another (the grantee) and includes a guarantee that the title is clear of undisclosed liens or claims. Regarding DSCR Loans, it’s most often needed when the ownership entity is changing as part of the transaction, i.e. acquisitions, but can also occur for DSCR Loan Refinances with Entity Changes, such as situations where the property is moving from one ownership structure to another, for example, from vested in personal name into an LLC or from one LLC to another. These types of refinance transactions may require a new Warranty Deed to reflect the change in vesting.

For DSCR Loans involving a Warranty Deed, the title company or closing attorney typically prepares the warranty deed and it is recorded with the county at the same time as the new mortgage/deed of trust. The grantor (current owner) signs the deed, and the grantee (new owner/entity) receives ownership subject to any liens listed in the title commitment. Note this is a standard part of the closing package in acquisitions.

Q: What is a warranty deed in a DSCR Loan closing?

A: A warranty deed is the legal document that transfers ownership of the property from one party to another and guarantees that the title is free of undisclosed liens or claims. In a DSCR loan, it’s always used in acquisitions to transfer title from the seller to you (or your ownership entity), and it may also be used in refinances if you’re changing the ownership entity, such as moving the property into an LLC. The warranty deed is prepared by the title company or closing attorney and is recorded in county records at the same time as your new mortgage or deed of trust.

A Release of Judgment or Lien Release is a recorded document that removes an outstanding claim from the property’s title records. For DSCR Loans, this is required any time a title search reveals that a judgment, tax lien, or other recorded lien is attached to the property. DSCR Lenders need to have a first-position lien from competing claims.

For an acquisition, if the title commitment shows a lien or judgment against the seller, the seller (through their title company) must pay off the debt and provide proof of release before closing. For refinances, the lien or judgment must be paid off and released by the borrower. Note that for either transaction type, the lienholder needs to issue a formal release, which the title company records to clear the lien from public records. The release must be recorded or guaranteed for recording before the final title policy is issued.

If a borrower has a recorded federal or state income tax lien and is currently repaying it through an official installment agreement, DSCR Lenders will typically require full documentation of the repayment plan. This is because tax liens, even for personal income taxes, can attach to all property owned and may take priority over the lender’s lien in the event of foreclosure (i.e. the IRS may be able to foreclose on the property to satisfy unpaid personal income taxes, ahead of the note holder of a DSCR Loan).

For a DSCR Lender to accept a Federal Income Tax Repayment plan for a borrower, there typically must be several key aspects of the plan that must be fully documented. The documentation will likely need to include total outstanding tax balance, the installment payment amount and due date and the repayment term and estimated payoff date There must also likely be confirmation the plan is current and in good standing and an official agreement from the IRS or state Department of Revenue.

Even though the DSCR Lender is the one who orders and manages the title work, borrowers still play a critical role in keeping the process on track. The title company can’t typically clear all requirements without borrower coordination leading up to close and delays here can cause issues. Best practices include to supply all entity documents neatly and quickly if borrowing through an entity (typically this will be the same entity document sets provided to the DSCR Lender, so no real extra documentation necessary).

Borrowers should also proactively resolve outstanding debts or charges, including any –past-due property taxes, recorded liens, judgments or HOA dues and sign curative documents if needed. These can include affidavits to correct name variations, corrective deeds to fix errors in past transfers, or other paperwork needed to clear title defects and often require notarization.

Investors (borrowers) should also proactively coordinate property access for required inspections or surveys. In some cases, the title insurer or lender may require a survey update or additional inspection to clear an exception. And as always, best borrower practice is to respond quickly to requests as many title clearance issues are time-sensitive, especially if they involve payoffs, lien releases or HOA documentation.

Up Next: Payoff Letters for DSCR Loans that are refinances on properties with existing debt.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.