.png)

.png)

By the time you’ve reviewed and signed the Term Sheet (or Letter of Intent, “LOI”), you’ve crossed a key threshold in the DSCR loan process. You’re no longer in the “just talking” stage, the DSCR Lender now has you on their live pipeline, and both sides are moving toward an actual closing.

This is where you’ll receive what’s often referred to as the needs list. Think of the needs list as your lender’s custom shopping list of documents and proof they must collect to move your file from “application” to “clear to close.” If the Term Sheet was the “handshake”, the needs list is the to-do list that makes the handshake closer to a done deal.

The lender now gets to work on building the complete loan file needed for underwriting, approval and eventual funding. That file will ultimately contain two categories of documentation. The first category of documentation includes items collected directly from you, the borrower (sponsor or guarantor). This is the “needs list” covered in this section. These are documents and proofs that you need to provide, such as ID, bank statements, leases and/or entity documents. The second category includes “lender-ordered” documents such as items ordered and managed by the lender from third parties. These include things like the appraisal, secondary valuation reviews and title policies. Your DSCR Lender will coordinate these directly with the providers, though they may need your cooperation for scheduling the payment.

This section focuses on the first category, the borrower-supplied documentation, or “needs list.”

From the borrower perspective, the needs list is the first real roadmap to closing, but it’s also the first point where a deal can get bogged down if you’re not organized. The speed and quality of the management of the needs list directly impacts whether you close on time and avoid any costly extension fees or lock expirations. Investors who treat this responsibility as urgent, and return complete and clearly labeled documents quickly, give themselves a major advantage in keeping the deal moving forward.

In this section, we’ll break down the core documents that are virtually always on the needs list for every DSCR deal as well as the conditional or “if applicable” documents that appear depending on the loan type and property specifics. We’ll also cover how the needs list differs between acquisitions and refinances and what “deal specifics” trigger extra documentation requirements. For example, if your property is a long-term rental with tenants in place versus a short-term rental (STR) you operate on Airbnb, or if it’s a condo versus a single-family residence (SFR) the list will differ. We’ll also cover how fees or costs typically fit into this stage, what’s “normal” and what’s not.

Typically, you’ll receive the needs list within one business day after the Term Sheet is signed. Many DSCR Lenders use a standard internal checklist and then tailor it to your file and will send over an initial needs list e-mail or link to an online portal that details the specific documents that you will need to provide.

.png)

Regardless of whether you’re buying or refinancing, and regardless of property type, there are a few categories of documents you can count on seeing every time. If you have these ready before you even receive the needs list, you’ll save valuable time. Prompt and well-organized needs lists responses will also be very appreciated by your DSCR Lender, and accrue possible benefits of priority and extra attention to processing your loan quickly. Check out each of the links below for all the details on the documents you'll need for every DSCR Loan.

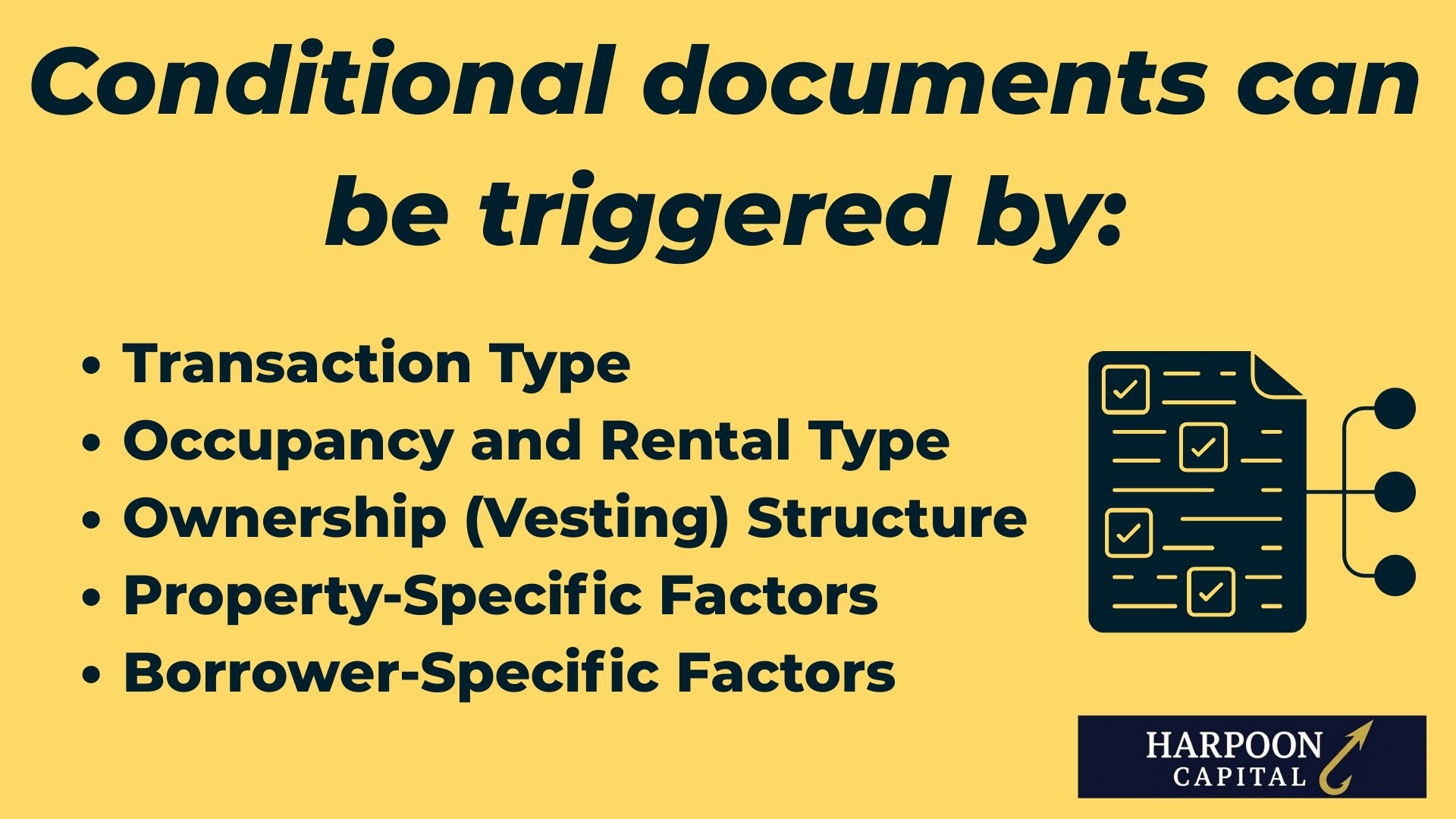

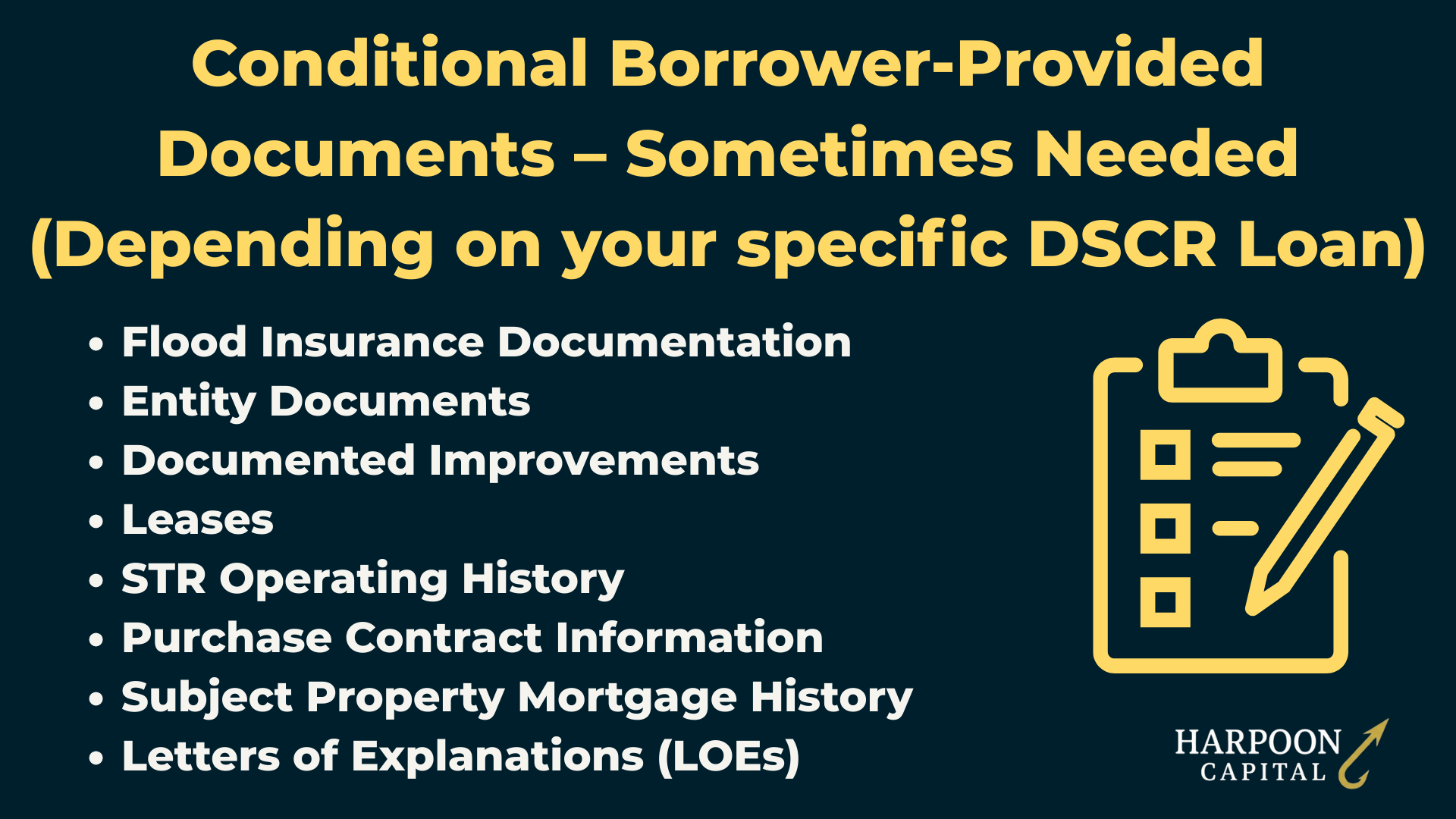

In addition to the core documents that appear on virtually every DSCR Loan needs list, there is a second category of items that are conditionally required. These documents are only requested when specific property characteristics, transaction types, or borrower situations trigger them.

Think of these as the “if applicable” items, they won’t apply to every DSCR Loan, but when they do, they’re just as important as the core documents in determining whether the loan can move forward. In some cases, these documents address risks unique to the property type (such as a condominium questionnaire), while in others they provide the lender with essential verification for a particular rental strategy or vesting structure (such as leases for in-place tenants or STR income history for short-term rental qualification or if the borrower is an LLC or Trust).

Conditional documents can be triggered by:

While the lender may initially label these as “only if applicable,” investors should treat them as priority items once requested. In practice, delays in obtaining conditional documents are one of the most common causes of slowdowns between signing a term sheet and submitting a complete loan file. Getting a head start on likely conditional requirements, based on your property and deal type, can shave days or even weeks off the closing timeline.

Inexperienced borrowers often treat the needs list as a “we’ll get to it” set of tasks. Experienced investors treat it as time-sensitive mission-critical work. Some borrower best practices include to respond in batches, meaning sending complete, organized batches of documents, not a drip of one attachment per email. An underrated, but very helpful practice for borrowers aiming for the smoothest and quickest DSCR Loan transactions is also to name files clearly such as “123 Main St – Bank Statement – June 2025.pdf” versus “scan003.pdf”. Some DSCR Lenders will have a secure portal where documents are dragged and dropped, while others may prefer e-mailed documents. How documents are sent rarely matters, as long as the documents are sent early, comprehensively and clearly labeled, you will be ahead of the curve. Any potentially tricky items, such as if you know your servicer is slow with questionnaires and VOM forms, or your STR reports have some quirks, ask and address a game plan for these proactively.

In addition, we provide a guide on Community Property State Signature & Consent Requirements for DSCR Loans that can come into play when providing needed documentation.

The needs list is a DSCR Lender’s blueprint for turning a signed Term Sheet into a funded DSCR loan. Handle it with the same urgency as the purchase contract deadlines in an acquisition or the rate-lock expiration in a refinance. Organized, fast document delivery can shave days or even weeks off your closing timeline and puts you at the top of a priority list, critical in competitive, fast-moving markets.

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.