.png)

.png)

In the mid-2000s, loose lending was king. Banks issued NINJA loans (“no income, no job, no assets”) and other so-called “no-doc loans” to borrowers with little verification. This led many Americans to dive headfirst into real estate investing through rental property loans with loose qualifications. Lured into false promises of getting-rich-quickly through real estate, and fed dreams of a life on easy mode, many real estate investors took on too many properties, too soon, with too much risk and leverage, rather than slowly building sound and stable rental property portfolios.

This house-of-cards approach contributed to the 2008 financial meltdown, By the 2010s, traditional mortgages had strict documentation rules under new Qualified Mortgage (QM) standards, which emphasized borrower income and ability-to-repay. This left lots of real estate investors in a tough spot: many had plenty of rental income potential but couldn’t qualify for conventional loans due to excessive qualifying hurdles, anti-entrepreneurial income and Debt-To-Income (“DTI”) requirements and strict limits on size and scope of portfolios.

Enter the DSCR loan – a loan option born in the late 2010s as a flexible financing solution for investors. DSCR Loans (short for Debt Service Coverage Ratio loans) are part of the “non-QM” mortgage universe. They offer a new era of real estate financing where the property’s cash flow, not the borrower’s personal income, serves as the primary qualifier. This guide will explore everything about DSCR loans, including what they are and how they work, how lenders determine rates and terms, a complete rundown of the loan process from start to finish as well as how DSCR Loans are becoming the go-to financing tools for innovative investing strategies such as short-term rentals or the BRRRR method. By the end, it will be clear why DSCR Loans have quickly become the favorite financing tool for investors building real estate portfolios and finding financial freedom!

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.

This guide will explain everything a real estate investor needs to know about DSCR Loans, the new gold standard for financing rental properties in the United States.

.png)

We will start with defining DSCR Loans in What Is a DSCR Loan and How Does a DSCR Loan Work?, providing a much-needed industry-standard definition for real estate investors, crucial in an industry notorious for an unsavory mix of acronyms, dual-meanings and confusing, gate-kept terminology. We will also break down a high-level overview on how DSCR Loans compare to Conventional Loans, or the loans guaranteed by government-sponsored entities that most homeowners and budding real estate investors are familiar with when it comes to mortgages.

This section includes an overview of DSCR Loan Structure Basics and advanced but crucially important provisions related to DSCR Loans such as Prepayment Penalties and Loan Rate Structure (Fixed vs. Hybrid Fixed to ARM). There is also a full breakdown of the Key Financial Metrics for DSCR Loans (Loan-To-Value “LTV” and DSCR ratios) to understand to be a well-equipped DSCR Loan borrower. Why do smart real estate investors use debt like DSCR Loans to build portfolios? The answer is covered in a breakdown of Real Estate Investing Returns and Using Leverage and cover the Basics of DSCR Loan Purposes (Acquisitions vs. Refinances). We will also walk through Common (and unfortunately persistent) Misconceptions and myths about DSCR Loans and set the record straight.

.png)

Following this overview, we’ll walk step by step through the process used by lenders to determine who qualifies for DSCR Loans and what are the ideal scenarios in which DSCR Loans make the most sense for a real estate investor. We’ll will walk through the “box” (industry jargon for lending parameters) for DSCR Loan Borrower Qualification, including experience, citizenship or visa and legal history requirements. We will also cover Financial Requirements for DSCR Loan Qualification, particularly down payment and liquid asset reserves requirements to access this type of financing. We will also cover Personal Financials and Credit Requirements for DSCR Loans including how mortgage lates, credit events (i.e. foreclosures, bankruptcies, short sales and deed-in-lieus) and judgments, liens, collections and charge-offs could affect or prevent qualification.

.png)

After covering the borrower requirements, we’ll tackle the other aspect of qualification: the property. First up, a comprehensive overview of DSCR Loan Property Type and Size Eligibility Requirements, including which types of properties are eligible for DSCR Loans (and which are not) as well as common square footage minimum requirements for each type of rental unit. Next is All About ADUs (Accessory Dwelling Units) for DSCR Loans, covering how qualification and eligibility work for this rental strategy that's been surging in popularity among investors. Full guides to DSCR Loans for Rural Properties and what to know about DSCR Lender "Declining Markets" categorization follow, as well as an overview of DSCR Loans for Condos, including a robust chart covering what could make a condo unit ineligible for DSCR Loan financing. This section concludes with Property Condition Rules for DSCR Loans and a guide to qualifying for DSCR Loans on properties with unorthodox leasing strategies (Property Usage and DSCR Loans) such as single room occupancy or medium term rentals.

Next comes a comprehensive look at How DSCR Lenders Determine Your Interest Rate, where we discuss how the different aspects of qualification work together to generate the interest rate and fees on your DSCR Loan quote, starting with the Three Key Factors That Determine Your Interest Rate and Terms(LTV, DSCR and FICO) and then explore Additional Factors for Determining Rate and Terms on a DSCR Loan that also have an impact. Then, we’ll take a peek “behind the curtain” of the exact process and tools DSCR lenders use to calculate your rate and terms, providing a step-by-step description and explanation, starting with Step 1: The Base Interest Rate Stack, then Step 2: Applying Loan-Level Price Adjustments (LLPA) to a DSCR Loan and conclude with a Step 3: Full Example for Pricing a DSCR Loan with a group of five quote options could be created for a typical DSCR Loan scenario.

In Section 5, we provide a detailed guide to becoming well-informed on Everything to Expect for Documents and Process for a DSCR Loan, from Stage 1 (Initial Quotes and Pre-Qualification) and Stage 2: Application and Credit Authorization to a fully closed and funded deal. We'll cover the DSCR Lender process of issuing Term Sheets or LOIs and Rate Locks (Stage 3) and then embark on a detailed breakdown of all the documents needed from borrowers, typically referred to as a Borrower "Needs List" (Stage 4). The detailed DSCR document breakdown begins with overviews of requirements for Identification, Financials (Liquid Assets and Reserves) and Property Insurance.

Continuing along the deep dive into DSCR Loan documents requirements, we'll cover Flood Insurance and Entity Documents (if borrowing through an entity, like an LLC). We'll also cover a common potential pitfall for DSCR Loan borrowers, nuanced rules and potential issues in terms of document and signature needs in Community Property States (Spousal Consent Guide). Next, we'll go through the requirement for Documented Improvements for refinances of properties that have been recently rehabbed, as well as Leases for long-term rental properties and Operating History (TTM Actuals) for active short-term rental properties. Additionally, we'll cover Purchase and Sales Agreements (PSAs) and Earnest Money Deposits (EMDs), relevant documents for DSCR Loans for purchase transactions.

For the last two borrower's needs list document deep dives, we'll take a close look at Subject Property Mortgage Histories, relevant for refinance loans where the property has existing debt and Letters of Explanations or "LOEs," often needed if there is a special or unique situation going on with a DSCR Loan deal, or if there is a blemish on background or credit that has an explanation that can provided needed context. Following all of the in-depth looks at the documents included in the borrower "needs list" (i.e. provided by the borrower), we'll move to Stage 5: Lender-Ordered Docs, other documents required for some or all DSCR Loans, but which are ordered and collected by the lender, not the borrower. This will include a comprehensive Guide to Appraisals for DSCR Loans as well as Secondary Valuation Reports (CDAs and Field Reviews) that also play a role in DSCR Loan underwriting. We'll also do a comprehensive Guide to Title Work for DSCR Loans as well as a quick look at Payoff Letters, a document necessary for lining up all the numbers on refinances where the new DSCR Loan is paying off an old debt.

Next, we will cover Condo Questionnaires for DSCR Loans, the extensive lender-ordered document that HOAs must fill out for DSCR Loans secured by condo rental units. Then, we'll move to Stage 6: Final Underwriting, where lenders determine the all-important Valuation Number Used for the LTV Ratio as well as the finalized DSCR Ratio, including how the Numerator (Revenue) of the DSCR Ratio is determined as well as the Denominator (PITIA) of the formula. Then, we'll move to Stage 7: Credit Approval and Clear To Close, when it is clear sailing to the finish line of a DSCR deal.

Approaching the finish line, we'll cover Tax & Insurance Escrow Calculations for DSCR Loans and then Drafting & "Balancing" the Settlement Statement. Then, we'll dive into the details of DSCR Loan Documents Drafting & Review, including highlighting the handful of states that have specific regulatory requirements that can add a day or two to the process. We'll next cover Stage 8: Closing and Funding and do a robust overview of all the Documents in a DSCR Loan Package. And we will conclude with Stage 9: Post-Closing and Ensuring DSCR Loan Servicing Success, with notes on how to make sure there are no mishaps in the months after close that might jeopardize your next DSCR deal.

We'll start this section with a Full History of How STR Financing has Evolved Over Time, with DSCR Loans emerging as the undisputed top option for STR Loans among real estate investors building short term rental portfolios. Then we'll do comprehensive comparisons for DSCR Loans vs. Conventional Loans for Short Term Rentals, DSCR Loans vs. 2nd Home Loans for Short Term Rentals and DSCR Loans vs. (Other) DSCR Loans for Short Term Rentals, or how different DSCR Lenders differ when it comes to financing STRs. Then, we'll wrap this section with all the answers to Advanced Lending Topics that STR Investors run into when financing growing short term rental portfolios, including questions and answers related to financing furnishings, how many bedrooms count for qualification and lender projections, how HOAs and local laws or regulations affect STR financing and if DSCR Loans can be used to finance unique hospitality properties like treehouses, yurts or other creative airbnbs.

DSCR Loans are also quickly becoming the top option for another real estate investing strategy that has taken off in recent years, the “BRRRR Method” (which stands for Buy Rehab Rent Refinance Repeat). We'll do a full overview of Using DSCR Loans for the BRRRR Strategy including complete comparisons and case studies for the BRRRR Method vs. Fixing and Flipping and the BRRRR Method vs. Traditional Buy-And-Hold. Then we’ll walk through All The Options For The Refinance Step of BRRRR why more and more investors are utilizing DSCR financing for the “refinance” portion of BRRRR over other options, especially since the 2023 decision by Fannie Mae extending the time investors need to wait to refinance their BRRRR method investments if using conventional loans.

Next, we'll explore how the popular DSCR Loan Product has Expanded In Recent Years past the traditional 1-4 unit residential limits to include small multifamily properties (up to 10 units) and even some mixed use properties including commercial units. These “Multifamily DSCR Loans” and “Mixed Use DSCR Loans” combine some of the best features of DSCR Loans, including easier qualification process and less paperwork, with achieving economies of scale with larger properties or properties with commercial uses. We will also provide an overview on how and why to use DSCR Loans for “Portfolios” of multiple properties, or “blanket loans” where multiple properties are combined or “cross-collateralized” to secure one DSCR Loan.

How to Track DSCR Loan Interest Rates provides a look at how real estate investors can track the “macro” or market-based portion of what makes up DSCR Loan interest rates, with an Overview of Bond Market Concepts and What Determines DSCR Rates? (Yes, Its Mostly the Fed). We do a comprehensive overview of The Data That Matters for DSCR Loan Rates and Decode "Fedspeak" or How Fed Meetings and Press Conferences Affect DSCR Loan Rates. We'll also include an overview of How to Understand Treasury Bond Auctions (and how those affect rates too) and conclude with a look at DSCR Loan Rates Over Time and a Future Rate Outlook.

In the final chapter: Who Offers DSCR Loans? we will do a full walk-though of the DSCR Loan Life Journey and cover all the entities and places a DSCR Loan is likely to go from origination to the long-term. We'll also cover The Mortgage Lending Ecosystem, where classifying different DSCR Lenders is more of a spectrum and mix-and-match rather than discrete boxes. There is a full guide to all The Players Involved: Entities and People You May Encounter in a DSCR Loan Transaction. Then we'll cover Brokering and Referring DSCR Loans and add a robustly researched Referral Rules Guide by State to cover where taking referral fees for DSCR Loans is for everyone and which states require licenses. Finally, we'll conclude with a specific guide for Referring DSCR Loans for Real Estate Agents, a group that is well equipped to learn about DSCR Loan and help refer their clients to lenders.

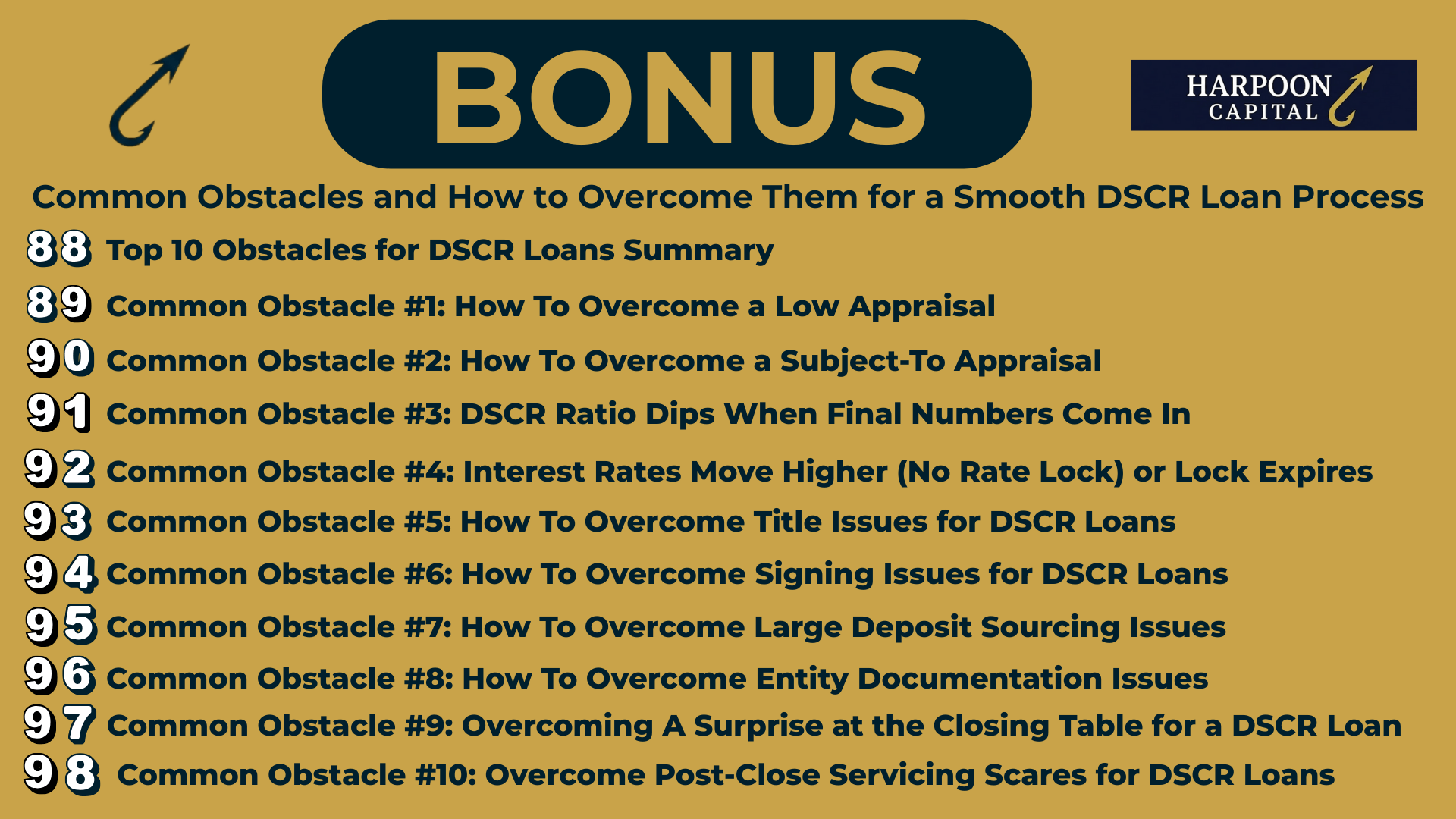

Finally, in one last BONUS section, we’ll describe 10 of the most common obstacles borrowers encounter that can derail a DSCR Loan and provide tips, tactics and strategies to prepare for and overcome them if they occur:

Common Obstacle #1 - Appraisal Value Comes in Low

Common Obstacle #3: DSCR Ratio Dips Below Threshold When Final Numbers Replace Estimates

Common Obstacle #4: Interest Rates Move Higher (No Rate Lock) or Lock Expires

Common Obstacle #5 – Title Issues for DSCR Loans

Common Obstacle #6 – Signing Issues for DSCR Loans

Common Obstacle #7 – Large Deposit Sourcing for DSCR Loans

Common Obstacle #8 – Entity Documentation Issues for DSCR Loans

Common Obstacle #9 – Surprise at the Closing Table for a DSCR Loan

Common Obstacle #10: Post-Close Servicing Scares for DSCR Loans

By the end of this guide you will know as much about DSCR Loans as any real estate finance professional, perhaps even more! Armed with this information and guidance, any investor will be ready to build cash-flowing rental property portfolios and chart their voyage to financial freedom with top knowledge and expertise on DSCR Loans, the best financing option out there for residential real estate investors!

© 2026 Harpoon Capital, LLC. All Rights Reserved. WARNING: Unauthorized distribution, copying, or sharing of this guide is a violation of U.S. Federal Law and is punishable by civil penalties of up to $150,000 per violation. We aggressively enforce our intellectual property rights.